This article was co-authored by Benjamin Packard. Benjamin Packard is a Financial Advisor and Founder of Lula Financial based in Oakland, California. Benjamin does financial planning for people who hate financial planning. He helps his clients plan for retirement, pay down their debt and buy a house. He earned a BA in Legal Studies from the University of California, Santa Cruz in 2005 and a Master of Business Administration (MBA) from the California State University Northridge College of Business in 2010.

There are 8 references cited in this article, which can be found at the bottom of the page.

This article has been viewed 992,681 times.

Getting out of debt and staying out of debt is not easy. Chances are, you're reading this article because you've already amassed a fair amount of debt and are thinking it will be impossible to ever get out from under it all. Learn how to stop incurring new debt and change your life forever.

Steps

Handling Your Credit Card Debt

-

1Lower your interest rates.[1] If you have good credit, contact the credit card companies and ask to have your rate lowered. That's an excellent way to lower your interest expenses and will save you money every month.

-

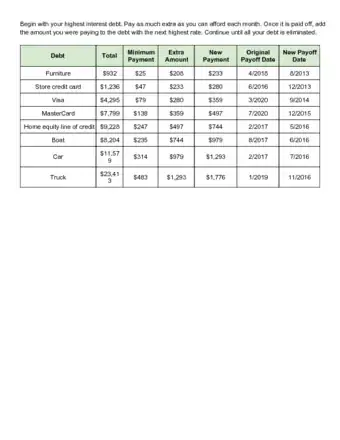

2Pay off your high interest credit cards first. If you can't get your interest rate lowered on some high interest credit cards, then pay those off first. That way, you'll reduce your interest expense over time by lowering the balance on those cards.[2]Advertisement

-

3Consider a debt consolidation loan. If your credit is good, you can consolidate your credit card debt into one debt consolidation loan. You'll find that it's easier to manage one payment per month than many payments. Plus, it's often the case that debt consolidation loans have a lower interest rate than credit cards.

-

4Stop using credit cards. To ensure that you get out of debt, you'll need to stop increasing your debt.[3] Switch from a credit card to a debit card so that the money you spend goes out of your account immediately.[4]

-

5Pay more than the minimum when possible. Credit card payments are structured to keep the cash flowing to the credit card companies for as long as possible. Avoid falling into a trap that hurts your financial position and helps your creditors by paying off more than the minimum payments whenever you can.

Managing Your Money

-

1Create a budget. If you're serious about getting out of debt, you need to track your income and expenses, so that you can discipline yourself to spend only what's necessary for any given month.[5]

- Make a list of all your sources of income. Include every way you earn money, whether it's from your job, investments, interest income, etc. Tally your various income streams by month.

- Make another list of your monthly expenses. Be sure to include everything you pay for every month, including utilities, groceries, gas, eating out, tuition, etc. Tally these expenses by month as well.

- Subtract your monthly expenses from your monthly income. If you have more income than expenses (and that should be the case), then the remainder is your discretionary income and can be used for debt relief or savings.

- Every month, be sure to stay within your budget. If you go outside of your budget, you'll have less money for debt relief or savings.

-

2Earn more money. To tackle your debt effectively, you're going to need more income. You can do that by either getting a second job (if you're a salaried employee) or earning more commissions (if you're in sales). Yes, this will take time away from your personal life, but it's necessary to get out of debt.

-

3Trim your expenses. Look for ways to reduce your expenses every month so that you have more money to pay off your debt.[6]

- Are you eating out too much? Save money by cooking your own food.[7]

- Can you reduce your utility bill with a more efficient use of energy? For example, does the downstairs area really need to be air conditioned while everybody is sleeping upstairs at night? Are there electrical devices left on all the time that shouldn't be?

- Consider extreme couponing to save money on your groceries.[8]

Seeing Professional Debt Relief Options

-

1Talk to a non-profit credit counselor. Your counselor will work with you to develop a plan to eliminate all of your debt and will contact your creditors to get the interest rate on your loans reduced.[9] You can find a non-profit credit counselor at the National Foundation for Credit Counseling website.[10]

-

2Consider a debt settlement. If your debt is totally out of control, your creditors might realize that some money is better than none. In that case, they might be willing to accept less than you owe rather than receiving nothing at all. In that case your debt to companies that accept your settlement will be eliminated entirely. For this option, you'll also need the assistance of a debt counselor.

- Be advised that this option will adversely affect your credit score. It will show up like a seriously delinquent payment or charged-off credit card debt.

-

3File for bankruptcy. One of the least attractive options to get out of debt is to file for bankruptcy because it severely impacts your reputation. However, you'll receive protection from your creditors and a judge might just make your debt go away entirely.[11]

- Consult with a professional bankruptcy attorney about this option.

- Keep in mind that you'll have a black mark on your credit report for about 7 years if you go this route.

Expert Q&A

Did you know you can get expert answers for this article?

Unlock expert answers by supporting wikiHow

-

QuestionWhat is the easiest way to save money?

Benjamin PackardBenjamin Packard is a Financial Advisor and Founder of Lula Financial based in Oakland, California. Benjamin does financial planning for people who hate financial planning. He helps his clients plan for retirement, pay down their debt and buy a house. He earned a BA in Legal Studies from the University of California, Santa Cruz in 2005 and a Master of Business Administration (MBA) from the California State University Northridge College of Business in 2010.

Benjamin PackardBenjamin Packard is a Financial Advisor and Founder of Lula Financial based in Oakland, California. Benjamin does financial planning for people who hate financial planning. He helps his clients plan for retirement, pay down their debt and buy a house. He earned a BA in Legal Studies from the University of California, Santa Cruz in 2005 and a Master of Business Administration (MBA) from the California State University Northridge College of Business in 2010.

Financial AdvisorTry to cut back on some of your expenses. For example, are you eating out too much? Save money by cooking your own food.

Support wikiHow by unlocking this expert answer.

-

QuestionHow do I get out of debt with no money?Benjamin PackardBenjamin Packard is a Financial Advisor and Founder of Lula Financial based in Oakland, California. Benjamin does financial planning for people who hate financial planning. He helps his clients plan for retirement, pay down their debt and buy a house. He earned a BA in Legal Studies from the University of California, Santa Cruz in 2005 and a Master of Business Administration (MBA) from the California State University Northridge College of Business in 2010.

Financial AdvisorOne option is refinancing. There are lots of great ways to refinance credit cards and student loan debt, for example. If you can lower the interest rate by just a single percentage point, it can have a big impact. In terms of saving, focus on little bits of progress. If your goal was to run a marathon, you wouldn't expect to run your first marathon in a week. For example, continue ordering out, but skip the glass of wine and appetizer. Try to practice intentional spending.Support wikiHow by unlocking this expert answer.

Warnings

- Be careful with those low-interest balance transfer credit cards. Their default rate will almost always get you into more debt.⧼thumbs_response⧽

- Check settlement companies to see whether they are registered with the BBB (Better Business Bureau). Examine whether there are several complaints filed against them, and whether those complaints were resolved.⧼thumbs_response⧽

- Try not to give too much personal information to a collections agency as everything you say is entered into a file. Keep the conversations short and sweet. Don't be tempted to answer personal questions and know your rights.⧼thumbs_response⧽

- Avoid the temptation of payday advance loans at all costs. It's a quick "fix" that will cause you to get into a snowballing problem of debt. Before you even think about taking out a payday loan, consider other resources: family and friends, home equity, and Debtors Anonymous.⧼thumbs_response⧽

- Don't be hasty. Closing revolving credit card accounts may actually lower your credit score. It can shorten the length of your reported credit history and make you seem less credit-worthy. Carefully choose which cards to cancel. You can avoid this problem by keeping the older cards and get rid of newer ones. However, you will still want to take your different rates into account as you choose which cards to cancel.⧼thumbs_response⧽

- Chronic spending and debt can be a harmful habit, just like alcoholism or any other addiction. Spending can be an escape, or can be used to mask deeper issues. Consult a professional and/or Debtors Anonymous if you feel you might have a problem.⧼thumbs_response⧽

References

- ↑ Benjamin Packard. Financial Advisor. Expert Interview. 11 March 2020.

- ↑ Benjamin Packard. Financial Advisor. Expert Interview. 11 March 2020.

- ↑ http://www.bankrate.com/finance/smart-spending/5-ways-to-cut-credit-cards-from-your-life-1.aspx

- ↑ Benjamin Packard. Financial Advisor. Expert Interview. 11 March 2020.

- ↑ http://www.moneycrashers.com/how-to-make-a-budget/

- ↑ http://www.thesimpledollar.com/trimming-the-fat-forty-ways-to-reduce-your-monthly-required-spending/

- ↑ Benjamin Packard. Financial Advisor. Expert Interview. 11 March 2020.

- ↑ http://www.livingwellspendingless.com/beginners-guide-to-coupons/thebeginners-guide-to-coupons-2/

- ↑ https://www.nfcc.org/

About This Article

To get out of debt, start by calling your credit card company and asking them to lower your interest rate. Then, pay off the cards with the highest interest rates first, trying to always pay more than the minimum. To avoid accruing more debt on those cards, make a budget for expenses and try to stick to it. Find ways to cut down on spending, such as using less energy at home or using coupons for groceries. If cutting expenses isn’t enough, you might consider getting another job to earn more income and pay down your debt. To learn more from our Financial Advisor co-author, like how to seek professional debt relief, keep reading!