This article was co-authored by Gina D'Amore. Gina D'Amore is a Financial Accountant and the Founder of Love's Accounting. With 12 years of experience, Gina specializes in working with smaller companies in every area of accounting, including economics and human resources. She holds a Bachelor's Degree in Economics from Manhattanville College and a Bookkeeping Certificate from MiraCosta College.

This article has been viewed 24,193 times.

If you do not file your taxes at all or you file them past the April 15 deadline, you may get a notice that you are being charged a penalty. The IRS may also penalize you if you cannot pay all of the taxes you owe. Though being charged with a penalty by the IRS can be stressful, you can pay it off online, by check, money order, wire transfer, or cash. Make sure you take steps to avoid paying penalties to the IRS in the future so you do not have to pay more than what you owe.

Steps

Determining How Much You Owe

-

1Pay a high failure-to-file penalty if you do not file your taxes on time or at all. If you do not file your taxes at all or file them late, you will be charged a penalty of 5 % of your unpaid amount each month the return is late. The penalty will kick in the day after the tax filing due date. However, the penalty will not exceed 25% of your unpaid taxes.[1]

- The failure-to-file penalty is often higher than if a failure-to-pay penalty so it is worth it for you to file your taxes in the long run, as you will end up paying a lower penalty.

-

2Budget for a failure-to-pay penalty if you cannot pay all of the taxes you owe. If you do not or cannot pay all the taxes you owe by the deadline, you will be charged a penalty of ½ of 1% of your unpaid taxes each month. The penalty begins the day after the tax-filing due date and will continue until you pay off your remaining balance to the IRS.[2]

- Try to pay off as much of the taxes you owe the IRS before the penalty kicks in, as this will make the penalty lower.

Advertisement -

3Try lowering the penalty if you have reasonable cause to do so. If you have a good reason why you did not file your taxes, such as a death in the family, a natural disaster, or an accident, contact the IRS to see if you can arrange a lower penalty. You can also request a lower penalty if you are in a financial bind, as the IRS will usually try to work with you to accommodate your situation.[3]

- If you are late to pay your taxes for the first time, you may qualify for a lower penalty through a first-time penalty abatement.[4]

- Talk to your accountant or a tax professional for advice on how you can get the penalty lowered.

Paying the Penalty

-

1Enroll in a payment plan if you cannot pay the penalty all at once. You can opt for a short-term payment plan as long as you owe less than $100,000 USD in taxes, penalties, and interest. If you need more time to pay the penalty, you can go for a long-term payment plan as long as you owe $50,000 USD or less and have filed all required tax returns. You will need to pay off the penalty in installments every month and you will be charged interest.[5]

- A short-term plan last 120 days or less and is free to set up. This is a good option if you feel you can get the funds to pay the penalty relatively soon.

- A long-term plan can last more than 120 days. It costs $31 USD to set up if you are paying with direct debit and $149 USD to set up if you are paying with debit, credit, check, or money order.

-

2Pay the penalty online through Electronic Federal Tax Payment System (EFTPS). The most secure way to pay any money owed to the IRS is through the EFTPS, which withdraws money from your bank account on a set date. You can enroll in EFTPS here: https://www.eftps.gov/eftps/.[6]

- It may take several days for your enrollment to go through so sign up sooner than later to avoid having to pay a higher IRS penalty.

-

3Use a check or a money order to pay the penalty. Make the check or money order payable to the U.S. Treasury. Include your name, address, phone number, Social Security Number (SSN) and the tax year with the check or money order. Send the check or money order to the address listed on the penalty notice you received in the mail from the IRS.[7]

- If you are paying the penalty in installments, send the check or money order to the address noted on your installments notice from the IRS.

-

4Pay the penalty with cash at the nearest IRS office. If you’d prefer to pay the penalty off in cash, do not send the cash through the mail. Instead, go in person to an IRS office to pay with cash. Bring exact change to make paying the penalty quick and easy.[8]

- Look for an IRS office near you here: https://apps.irs.gov/app/officeLocator/index.jsp.

- You can also pay off the penalty in installments in cash by going in person to the IRS office.

Avoiding Future Penalties

-

1Try to file your taxes early. The best way to avoid a failure-to-file penalty or a late fee is to always file your taxes before the deadline each tax year. Put the tax deadline in your calendar and prepare your tax documents several weeks early so you do not have to worry about missing the deadline.[9]

- If you use an accountant to help you file your taxes, you may make an appointment with them several weeks before the due date so you file your taxes on time.

- Do not skip filing your taxes, even if you are going to file them late, as this can lead to a steeper penalty.

- Remember that the tax deadline is December 31. April 15 is the deadline for tax paperwork, not tax payment.

-

2Pay as much of your taxes as you can to avoid a high penalty. If your taxes are more than you can afford, try to pay off as much as you can manage. Then, enroll in a short-term payment plan and try to pay the rest off as fast as you can to avoid paying a high penalty and interest. Addressing the taxes and penalties you owe right away will ensure you do not end up paying a high amount to the IRS.

- Late payments interest is calculated daily, so you have to keep that in mind, especially if you're writing a check, since the interest will keep growing.

-

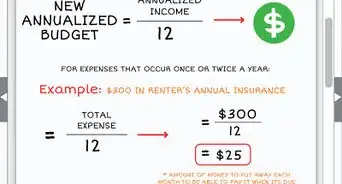

3Set aside money in a savings account so you can pay your taxes in full. Plan ahead by putting aside a percentage of your earnings into a savings account so you can cover the taxes you will owe for the tax year. The percentage will depend on your income bracket, as the higher the income bracket, the higher the percentage you will owe. Try to put more than you think you will owe so you are covered when it comes to paying your taxes in full. This will allow you to avoid high penalties.[10]

- You can sign up for automatic withdrawals to your savings account each month through your bank so you do not have to worry about doing it yourself.

References

- ↑ https://www.irs.gov/newsroom/eight-facts-on-late-filing-and-late-payment-penalties

- ↑ https://www.irs.gov/newsroom/eight-facts-on-late-filing-and-late-payment-penalties

- ↑ https://www.irs.gov/newsroom/eight-facts-on-late-filing-and-late-payment-penalties

- ↑ http://www.taxdebthelp.com/tax-problems/unpaid-taxes/failure-to-pay-penalty

- ↑ https://www.irs.gov/payments/online-payment-agreement-application

- ↑ https://www.irs.gov/payments/eftps-the-electronic-federal-tax-payment-system

- ↑ https://www.irs.gov/payments/pay-by-check-or-money-order

- ↑ https://www.irs.gov/payments/pay-by-check-or-money-order

- ↑ https://www.irs.gov/newsroom/eight-facts-on-late-filing-and-late-payment-penalties

About This Article