This article was co-authored by Jonathan DeYoe, CPWA®, AIF® and by wikiHow staff writer, Jennifer Mueller, JD. Jonathan DeYoe is a Financial Advisor and the CEO of Mindful Money, a comprehensive financial planning and retirement income planning service based in Berkeley, California. With over 25 years of financial advising experience, Jonathan is a speaker and the best-selling author of "Mindful Money: Simple Practices for Reaching Your Financial Goals and Increasing Your Happiness Dividend." Jonathan holds a BA in Philosophy and Religious Studies from Montana State University-Bozeman. He studied Financial Analysis at the CFA Institute and earned his Certified Private Wealth Advisor (CPWA®) designation from The Investments & Wealth Institute. He also earned his Accredited Investment Fiduciary (AIF®) credential from Fi360. Jonathan has been featured in the New York Times, the Wall Street Journal, Money Tips, Mindful Magazine, and Business Insider among others.

This article has been viewed 258,172 times.

Annualization is a predictive tool that estimates the amount or rate of something for an entire year, based on data from part of a year. This tool is primarily used for taxes and investments. If you're paying estimated taxes, you'll need to annualize your income to determine how much tax to pay. With investments, you can annualize your rate of return to help choose your investment strategies. However, you can also use this tool to create a yearly budget for yourself or your household.[1]

Steps

Annualizing Your Income

-

1Gather income reports for 2 or 3 months. To annualize your income, you need a sample of the income you earn over a year. You can get this from paystubs, paid invoices, or even your bank statement.[2]

- If your income is extremely regular, you may not need more than a month of income to complete an annualization.

- If you receive income from multiple sources, make sure you have information for all sources you want to include.

-

2Total your income for the period. It's easiest to annualize income using months. Add up your income from all sources to get your total income for that period of time. Make a note of how many months of income you used to get that total.[3]

- For example, suppose you have 3 monthly paychecks of $7,000, $6,500, and $6,800. Your total would be $20,300 of income over a 3-month period.

Advertisement -

3Divide the number of months in a year by the months of income. To annualize your income, use the ratio of the number of months in a year (12) over the number of months in the period you used to get your total. When you divide, your result will always be a number greater than 1.[4]

- For example, if you totaled your income over 3 months, your ratio would be 12/3 = 4.

-

4Multiply your total income by the result of the ratio. Once you've divided the ratio, multiple the total income you found for the period by that number. The result will be the estimated amount of income you earn in a year.[5]

- For example, if your total income over a 3-month period was $20,300, your annualized income would be $20,300 x 4 = $81,200.

- You may not have to annualize your income to pay estimated taxes. For example, in the US, you pay estimated taxes based on your actual income for that quarter – not what you project you'll earn later.

Determining an Annualized Rate of Return

-

1Familiarize yourself with the formula. The formula to calculate an annualized rate of return (ARR) may look fairly intimidating at first. However, once you break it down into pieces, it's not as difficult as it looks.[6]

- The full formula is ARR = (1 + rate of return per period)# of periods in a year – 1. The 1 simply turns a percentage into a whole number so you can compound it. That's why it's subtracted at the end to get your final rate.

- Essentially, all you do is compound the rate of return by the number of periods. If you have a monthly rate of return, you would compound the rate by 12. A weekly return would be compounded by 52, while a daily return would be compounded by 365.

-

2Calculate your rate of return. To calculate the rate of return on your investment, subtract the ending value of your investment from the beginning value of your investment, then divide that number by the beginning value of your investment. Multiply the result by 100 to get your rate of return.[7]

- For example, if you set up a portfolio with $10,000, and it now has a balance of $11,025, you have a total gain of $1,025. According to the equation, your rate of return is (11,025 – 10,000 / $10,000) x 100 = 10.25%.

-

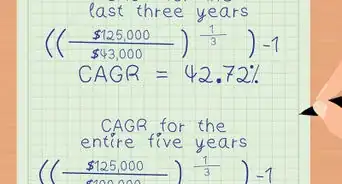

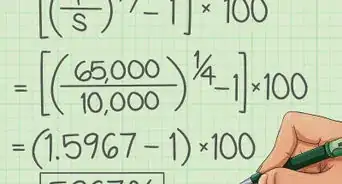

3Determine the period to which your rate of return applies. Quantify the period of time over which you had the gain. Then divide (usually 365, the number of days in a year) by that number to find out how many of those periods are in one year.[8]

- For example, suppose you had a 10.25% rate of return on an investment that was 65 days old. The number of 65-day periods in a year is 365 / 65 = 5.615.

- If your rate of return happened to be a single day or a single month, you can skip this step and compound your rate of return by 365 (days) or 12 (months).

-

4Compound your rate of return by the number of periods in a year. Place the number of periods in a year in the formula to annualize your rate of return. Complete the calculation using the xy button on your calculator.[9]

- For example, your equation for the ARR continuing the example would be (1 + 0.1025)5.615 – 1 = 0.7296 or 72.96%. Your annualized rate of return on the investment, therefore, is 72.96%.

- There are significant limitations to an annualized rate of return. Specifically, you have no guarantee that you'll be able to continually reinvest the money at the same rate.

Creating a Yearly Budget

-

1Gather records of financial transactions for a 2- or 3-month period. Typically, a few months of bank statements is all you need to annualize expenses and create a yearly budget. If you frequently use a credit card, get copies of your credit card statements for the same month.[10]

- Use income and expenses across the same time period. In other words, if you annualize 3 months of income you should also annualize 3 months of expenses.

-

2Annualize your income. Total your income over 2 or 3 months. Then multiply that total by the ratio of the number of months in a year over the number of months of income. This provides you with the amount of income you make each year.[11]

- For example, suppose you have 3 monthly paychecks of $4,200, $5,100, and $4,700, for a total of $14,000. Your annualized income would be $14,000 x 12/3 = $14,000 x 4 = $56,000.

- Be sure to include any other sources of income in your equation. If you have any money that you only receive once a year, such as a bonus, you can simply add it into your annualized income.

-

3Organize your expenses into categories. You can make as many categories as you want. A broad category, such as "bills," likely won't be very helpful if you want to figure out where your money's going. On the other hand, too many individual categories add work and can get confusing.[12]

- For example, you might have categories such as "house payment," "utilities," and "car." Under "utilities," you would include bills such as electricity, gas, telephone, trash, and water and sewer. Under "car," you might include your car payment, car insurance, and fuel.

- If there are specific expenses that you think are getting out of control, or that you want to keep particular tabs on, make them their own category. For example, assume you believe that you're spending too much money buying lattes from the café near your work. You might create a "latte" category specifically for that expense.

-

4Identify the time period for each expense. To annualize your data, you have to know how often the expense occurs. Many recurring bills are monthly. However, you may have some that are every other month, every quarter, or only twice a year.[13]

- You'll also have expenses that are daily or weekly, or that happen a few days a week. For example, if you get fuel for your car once every other week, the time period for that expense for the purposes of your annualization equation would be 52 / 2 = 26.

- Expenses that only occur once or twice a year don't have to be annualized. Simply add them into your annualized total.

-

5Annualize expenses based on the data you have. Take the same formula you used to annualize your income and use it to annualize your expenses. Then total the annualized expenses in each category.[14]

- If you have several expenses in one category that all have the same time period, you can annualize them together. For example, if your car payment and your car insurance payment are both monthly expenses, you could total them and only make one calculation.

-

6Make adjustments where necessary to balance your budget. Financial experts recommend budgeting your money so that 50% of your income goes towards necessities, 20% towards things that you want, and 20% towards savings for the future. Organize your categories into these broader categories and see how your annualized numbers compare.[15]

- If this is your first time doing an annualized budget, you may find that the proportions are far off track from where they need to be. Balancing a budget takes time and effort.

- Identify problem expenses that you think you can decrease or eliminate entirely. For example, if you have a subscription to a magazine that you never read, you can save that cost by simply canceling the subscription.

-

7Create a new budget based on your results. Once you've made your adjustments, take your annualized income and divide it by 12 to figure out how much money you have to work with each month. Then put in your expenses.[16]

- For expenses that only occur once or twice a year, divide the total expense by 12 to determine the amount of money you should put towards that expense each month so that you're ready to pay it when it's due. For example, if you pay $300 in renter's insurance once a year, you would need to put away or earmark $25 each month.

Expert Q&A

-

QuestionIs annualized return good?

Jonathan DeYoe, CPWA®, AIF®Jonathan DeYoe is a Financial Advisor and the CEO of Mindful Money, a comprehensive financial planning and retirement income planning service based in Berkeley, California. With over 25 years of financial advising experience, Jonathan is a speaker and the best-selling author of "Mindful Money: Simple Practices for Reaching Your Financial Goals and Increasing Your Happiness Dividend." Jonathan holds a BA in Philosophy and Religious Studies from Montana State University-Bozeman. He studied Financial Analysis at the CFA Institute and earned his Certified Private Wealth Advisor (CPWA®) designation from The Investments & Wealth Institute. He also earned his Accredited Investment Fiduciary (AIF®) credential from Fi360. Jonathan has been featured in the New York Times, the Wall Street Journal, Money Tips, Mindful Magazine, and Business Insider among others.

Jonathan DeYoe, CPWA®, AIF®Jonathan DeYoe is a Financial Advisor and the CEO of Mindful Money, a comprehensive financial planning and retirement income planning service based in Berkeley, California. With over 25 years of financial advising experience, Jonathan is a speaker and the best-selling author of "Mindful Money: Simple Practices for Reaching Your Financial Goals and Increasing Your Happiness Dividend." Jonathan holds a BA in Philosophy and Religious Studies from Montana State University-Bozeman. He studied Financial Analysis at the CFA Institute and earned his Certified Private Wealth Advisor (CPWA®) designation from The Investments & Wealth Institute. He also earned his Accredited Investment Fiduciary (AIF®) credential from Fi360. Jonathan has been featured in the New York Times, the Wall Street Journal, Money Tips, Mindful Magazine, and Business Insider among others.

Author, Speaker, & CEO of Mindful MoneySpeaking about annualized portfolio return, it gives an investor a sense of how a portfolio has performed from the point the calculation starts until the moment the calculation ends on an average annual basis. It is not a very useful measure if you have only been invested for 18 months — there is not enough information to tell you anything valuable. It becomes more useful when you are looking at longer periods of time. -

QuestionI use QuickBooks, and a board member ask for an annualized profit and loss report. Is that just a year-long profit and loss report from January to December?

DonaganTop AnswererYes, "annualized" refers to a one-year period, typically January through December.

DonaganTop AnswererYes, "annualized" refers to a one-year period, typically January through December. -

QuestionHow do you annualize sales?

Drew Hawkins1Community AnswerStart by gathering income reports for a 2-3 month period to use as a sample. For instance, you can use pay stubs, invoices, or even your bank statement. Add up your income for the sample period and make a note for the total number of months you used to get that amount. Then, divide the number of months in a year by the months of income. Multiply your total income by the result to find your annualized income for the year.

Drew Hawkins1Community AnswerStart by gathering income reports for a 2-3 month period to use as a sample. For instance, you can use pay stubs, invoices, or even your bank statement. Add up your income for the sample period and make a note for the total number of months you used to get that amount. Then, divide the number of months in a year by the months of income. Multiply your total income by the result to find your annualized income for the year.

References

- ↑ https://www.investopedia.com/terms/a/annualize.asp

- ↑ https://www.investopedia.com/terms/a/annualized-income.asp

- ↑ https://www.investopedia.com/terms/a/annualized-income.asp

- ↑ https://www.investopedia.com/terms/a/annualized-income.asp

- ↑ https://www.investopedia.com/terms/a/annualized-income.asp

- ↑ https://financetrain.com/how-to-calculate-annualized-returns/

- ↑ https://www.readyratios.com/reference/analysis/annualized_rate.html

- ↑ https://www.readyratios.com/reference/analysis/annualized_rate.html

- ↑ https://financetrain.com/how-to-calculate-annualized-returns/

- ↑ https://www.investopedia.com/university/guide-to-planning-a-yearly-budget/creating-a-yearly-budget.asp

- ↑ https://www.investopedia.com/university/guide-to-planning-a-yearly-budget/creating-a-yearly-budget.asp

- ↑ https://www.investopedia.com/university/guide-to-planning-a-yearly-budget/creating-a-yearly-budget.asp

- ↑ https://www.investopedia.com/university/guide-to-planning-a-yearly-budget/creating-a-yearly-budget.asp

- ↑ https://www.investopedia.com/university/guide-to-planning-a-yearly-budget/creating-a-yearly-budget.asp

- ↑ https://www.nerdwallet.com/blog/finance/how-to-build-a-budget/

- ↑ https://www.nerdwallet.com/blog/finance/how-to-build-a-budget/

About This Article

to annualize your income, which is when you estimate its amount for an entire year based on information from a few months, start by gathering information for 2 or 3 months. For example, if you want to calculate your annual pay, find pay stubs for 3 months. Then, add up the total income you got during the period, and note down how many months it covered. Once you’ve finished your calculation, divide the number of months in the year by the number of months in the period of your records, which in the example would be 12 divided by 3. Finish by multiplying your total income by the result of the ratio, which in this case would be 4. For tips on how to calculate annualized returns, keep reading!