This article was co-authored by Brian Colvert, CFP®. Brian Colvert is a Certified Financial Planner and the CEO of Bonfire Financial. With over 15 years of experience in finance, he specializes in helping others plan for a secure and confident financial leap into retirement. Brian holds a BA from San Diego State University.

There are 7 references cited in this article, which can be found at the bottom of the page.

This article has been viewed 228,446 times.

An annuity is an insurance contract that takes the form of an investment. Annuities provide an income source with periodic payments for an agreed-upon period of time for the annuitant or their beneficiary, beginning now or at some point in the future. Understanding how your annuity works will help you plan for the future and adjust your other investments accordingly.

Steps

Determining the Type of Annuity You Have

-

1Determine the type of payout of your annuity. Check your paperwork or call the issuing firm to find out whether your payout is immediate or deferred. If it is an immediate annuity, the payments will begin immediately after your initial investment. If you have a deferred annuity, it will accumulate regular rates of interest.[1]

-

2Determine the investment type of your annuity. Your investment may be fixed or variable—you can also check your paperwork or call the issuing firm to find out this information, as there's usually a rider with a predetermined percentage to paid. A fixed annuity will have a guaranteed rate of interest, and therefore a guaranteed payout. A variable annuity depends heavily on the performance of its underlying investments and therefore offers payouts that may vary from month to month. You choose the investments at the time you purchase the annuity. This annuity is also tax-deferred.[2] [3]Advertisement

-

3Know your liquidity options. Check your annuity contract or call the issuing firm to find out your annuity's liquidity options—it may have penalties for early withdrawal and you might end up with less money. Some annuities with withdrawal penalties may allow you to withdraw a portion without penalty, however, while other annuities may be available without any withdrawal penalty, such as no-surrender or level-load annuities.[4]

Determining the Details of Your Annuity

-

1Find out your annuity's payout option. The most popular payout option pays the full amount of the annuity over a specified period, with any balance remaining after your death being paid to your beneficiary. Other options will pay out until death with no beneficiary or pay out for a certain period including payments to your beneficiary for the duration of the period after your death. Still another option pays out to the beneficiary for the duration of his or her life beyond your own.[5]

-

2Find out the principal balance. Your principal balance is the amount you pay to purchase the annuity either as an initial payment or as a monthly contribution (such as from your paycheck).[6] If you make payments on a regular basis, you will have to inquire as to the current balance in order to calculate your payments.

- You should also receive statements on your annuity, which should list your principal balance.

-

3Find out the interest rate. There may be a guaranteed minimum interest rate that you may receive when you purchase your annuity, which means your interest rate will never fall beneath that rate.[7] Otherwise, a fixed rate should be noted in the paperwork you received when you purchased the annuity, or, if it is variable, you should be able to call the provider or check your account online to find your interest rate.

- Your statement should also list your interest rate.

Calculating Your Payments

-

1Calculate the amount of the payments based on your specific situation. For example, assume a $500,000 annuity with a 4% interest rate that will pay a fixed annual amount over the next 25 years. The manual formula is Annuity Value = Payment Amount x Present Value of an Annuity (PVOA) factor.

- The PVOA factor for the above scenario is 15.62208. Thus, 500,000 = Annual Payment x 15.62208. Solving the equation for the annual payment gives us $32,005.98.

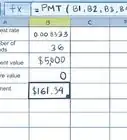

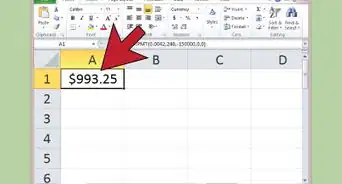

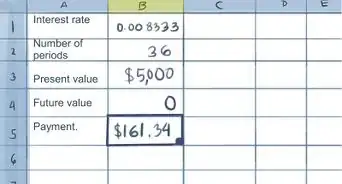

- You can also calculate your payment amount in Excel using the "PMT" function. The syntax is "=PMT(Interest rate,Number of periods,PresentValue,FutureValue)." For the above example, type "=PMT(0.04,25,500000,0)" in a cell and press "Enter." There should be no spaces used in the function. Excel returns the value of $32,005.98.

-

2Adjust your calculation if your annuity will not begin paying out for several years. Find the future value of your present principal balance by using a Future Value table,[8] the rate of interest that will accrue on your annuity between now and when it begins to pay out, and the number of years until you begin drawing payments. For instance, assume that your $500,000 will earn 2% annual interest until it begins paying out in 20 years. Multiply 500,000 by 1.48595 as per the FV factor table to find 742,975. Future values are created using mathematical equations—you can find a link to a table here.

- Find the future value in Excel by using the FV function. The syntax is "=FV(InterestRate,NumberOfPeriods,AdditionalPayments,PresentValue)." Enter "0" for the additional payments variable.

- Substitute this future value as your annuity balance, and recalculate the payment using the formula "Annuity Value = Payment Amount x PVOA factor". Given these variables, your annual payment would be $47,559.29.

Warnings

- Financial advisors agree that no one should rely on a single income source for support in retirement. Diversification (having several sources) is crucial in any investment portfolio.⧼thumbs_response⧽

References

- ↑ http://www.annuityfyi.com/types-of-annuities/

- ↑ https://money.cnn.com/retirement/guide/annuities_fixed.moneymag/

- ↑ http://money.cnn.com/retirement/guide/annuities_variable.moneymag/index.htm?iid=EL

- ↑ http://www.annuityfyi.com/types-of-annuities/

- ↑ http://money.cnn.com/retirement/guide/annuities_basics.moneymag/index8.htm

- ↑ http://financial-dictionary.thefreedictionary.com/Annuity+Principal

- ↑ https://www.usaa.com/inet/pages/insurance_annuities_flex_retirement?akredirect=true

- ↑ http://highered.mcgraw-hill.com/sites/dl/free/0072994029/291202/4eFutureValueof1_table1.pdf

About This Article

Before calculating your annuity payments, figure out if you have an immediate or deferred payout. Then, determine whether your investment will be fixed or variable. To calculate your annuity, use the PMT function in excel or multiply the payment amount times the present value of an annuity factor. For help understanding your liquidity options and interest rates, read more from our Financial reviewer.