This article was co-authored by Derick Vogel. Derick Vogel is a Credit Expert and CEO of Credit Absolute, a credit counseling and educational company based in Scottsdale, Arizona. Derick has over 10 years of financial experience and specializes in consulting mortgages, loans, specializes in business credit, debt collections, financial budgeting, and student loan debt relief. He is a member of the National Association of Credit Services Organizations (NASCO) and is an Arizona Association of Mortgage Professional. He holds credit certificates from Dispute Suite in credit repair best practices and in Credit Repair Organizations Act (CROA) competency.

There are 19 references cited in this article, which can be found at the bottom of the page.

wikiHow marks an article as reader-approved once it receives enough positive feedback. In this case, 80% of readers who voted found the article helpful, earning it our reader-approved status.

This article has been viewed 312,719 times.

Credit reports are used by banks, credit card issuers, car dealerships, landlords, and even employers to determine your reliability for credit. With so much riding on it, you naturally want your score to be as high as possible. Unfortunately, mistakes can happen and your score might not be as high as you'd like it to be. Don't panic! There are some simple steps you can take to raise your credit rating, as well as many things you can do to keep your credit score high in the future.

Note: This article applies to the United States. While some of the information here is relevant for other jurisdictions, check with your relevant local sources to verify first.

Steps

Your Credit Situation

-

1Learn how your credit score is calculated. There are three national credit bureaus TransUnion, Equifax and Experian that calculate your credit score, and your score can differ depending on the agency, as they may have differing information about your credit history.[1] There are five major components to your credit score. Each of them is weighted differently.[2]

- Payment history (35%) — The most important component of your credit score is your payment history. Do you pay your bills on time? Do you have a history of late payments? If so, how late? Have you ever been turned over to collections? You can expect that late payments will deduct points from your score.[3]

- Amounts owed (30%) — What's your overall debt load? If you've taken on too much debt, your score could suffer.

- Length of credit history (15%) — How long is your record when it comes to managing credit? If you're brand new to the scene, then lenders will view you as a risky borrower compared to someone who's been paying off debt for decades.

- New credit (10%) — Taking out a bunch of new loans and/or opened credit card accounts will reduce your score.

- Types of credit (10%) — A healthy mix of debt (a mortgage, a credit card, and a car loan) is viewed a little more favorably than debt consisting entirely of credit cards. However, don't open a new credit account just to have "balance." Instead, focus on the other components of your score.

-

2Know how your credit score influences loans. When you are looking to take out a loan, perhaps for a mortgage or to buy a car, lenders are going to look at your credit score to help them determine if you are reliable enough to pay back the loan. They will also use your credit score to help them determine the interest rate on a loan. If you have a high credit score, you will likely qualify for lower interest rates.[4] A low score may mean a higher interest rate, or even being denied a loan.

- Different lenders may use industry-specific scores. For instance, a credit card company may look at your FICO Bankcard Score, or an auto lender may order your FICO Auto Score, to give them a more specific look at your relevant credit information.[5] When applying for a personal loan, student loan, or mortgage, your lender may examine your credit score from all three bureaus.[6]

Advertisement -

3Request your credit report from the three national credit bureaus. If you need to fix your credit score, then reviewing your credit report is the best way to see what you need to do. Your credit report gives you a full history of your transactions and credit usage. Contact Experian, Equifax, and TransUnion to get a report from each of them.[7]

- The contact information for TransUnion, Equifax and Experian can be obtained online at their websites or from the Credit Info Center.

- You can obtain one free credit report per year from each of the three agencies. Request one report every four months so you can continually monitor your reports. Your credit history is free but you may have to pay a small cost to get your actual credit score. Some banks and credit unions offer credit score information to their customers for free.[8]

- Free websites like Credit Karma don't always provide accurate information.[9] Some free services are scams and will stand there between you and the credit companies in order to harvest your data and then sell the data to marketing firms.

-

4Review your credit report to find areas that you can improve. Your credit report will give you a full history of your credit transactions. If your score needs improvement, then go through your report very carefully to see what's pulling your credit down. This way, you'll know what you need to fix. Some common problems include:[10]

- Regularly paying your bills late.

- Outstanding or unpaid bills, or bills that have been sent to collections.

- Maintaining a debt to credit ratio higher than 30%.

- Multiple credit inquiries within a short period of time.

Debt Management

-

1Keep your debt ratio below 30% of your credit limit. A major part of your credit score is your outstanding debt load. While some debt is fine, outstanding debt of over 30-35% of your credit limit will impact your score. Either keep your debt below this limit, or start paying down your outstanding debt to lower it.[11]

- If you have a $10,000 credit limit and have a $4,000 balance, that means 40% of your credit line is used.

- This also counts for any single one of your cards or credit sources. If you have 3 cards with no balance but 1 card that’s 60% used, this could have a negative impact on your score.

- If you make large purchases one month, like an expensive vacation, your score will decrease. The score should increase again once you pay off the balance, so make sure you only charge what you can afford to pay off.

- Keeping your debt ratio below 10% of your credit limit is even better. Studies have found that people with high credit scores usually only use around 7% of their credit limit.[12]

-

2Prioritize paying off any past-due bills first. Outstanding bills are a real drain on your credit score. Furthermore, the older these unpaid bills are, the more they’ll reduce your score. If you have any unpaid bills, take care of those first. Once they’re gone, your credit score can start improving.[13]

- It’s best to pay off late bills in full, but if you don't have enough cash on hand to do that, pay what you can to start reducing your outstanding debt.

- If you're paying off debts, try the avalanche technique. Pay off the debt with the highest interest rate first. Then work your way down from the highest interest rates to the lowest.

- You can also try the snowball technique. With this method, you pay off your smallest debt first and work your way up. This is not always the most efficient way to pay off your debts in terms of saving money, but the sense of accomplishment that comes with successfully paying off a debt, even a small one, can help motivate you to keep at it.

-

3Pay all your bills on time from now on. Paying bills late, whether on purpose or accidentally, is one of the main ways that people hurt their credit scores. Make a commitment to pay all of your bills on time from now on. This establishes a good credit history that will improve your score before too long.[14]

- Even just one late payment could affect your credit score by 50-100 points.[15]

- If you have trouble remembering to pay bills, set reminders to go off on the day your bills are due.

- You could also set up automatic payments. This way, the money will automatically transfer from your account to the credit card without you having to do anything. Just make sure you keep enough money in your account.

-

4Make more than the minimum payments if you can, to reduce your debt load faster. Making minimum payments means that you’ll pay down your debt more slowly, so it’ll take time for your score to improve. Furthermore, you’ll keep accruing interest on your balances, so you’ll end up paying more in the long run. [16]

- Most credit cards have a relatively small minimum, like $25. However, if you have $1,000 of debt, it’ll take a long time to pay that down with minimum payments, and you’ll pay high interest while you do.

- If you can only afford to make minimum payments, it's still better than nothing, and it avoids late fees.

-

5Stop using your credit card if you have a lot of debt. If you’re already carrying a lot of debt, then adding to it could reduce your credit score further. In this case, it’s best to switch to using cash instead. That way, you’ll avoid adding more to your balances while paying them down gradually.[17]

- Using cash is also a good way to stop yourself from spending too much. People usually spend more when they use credit cards instead of cash.

-

6Be patient while your score improves. Even if you make all these positive changes, it still takes some time for your credit score to improve. Credit improvements usually take about 3-6 months to show up on your credit report and affect your score. In the meantime, continue budgeting and practicing good credit habits to improve your score as much as possible.[18]

Good Credit Habits

-

1Ask for a credit limit increase to reduce your debt ratio. If your credit cards have a low limit, then you might have a high debt ratio, which hurts your score. In this case, you can ask the credit card company for a limit increase. Ask long as you don’t put a higher balance on the card, this will reduce your debt ratio.[19]

- If your card has a $1,000 limit and you have $500 on it, then your debt ratio is 50%. However, if you get the limit increased to $2,000, then the ratio falls to 25%.

- Only do this if you know you can resist over-spending. Getting a limit increase but then maxing out the card won’t help you.

- You could also increase your total limit by getting a new card, but applying for new cards could decrease your score.

-

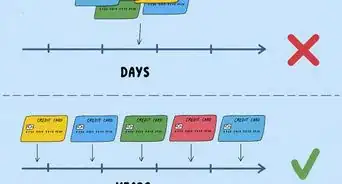

2Keep unused cards and accounts open to build your credit history. Your credit history makes up 15% of your credit score. The longer you have a line of credit, the more your score improves. Keeping older cards open maintains your credit history and improves your score, even if they're unused.[20]

- If, however, you have problems with temptation, it’s worthwhile to close unused cards, so you won’t be tempted to overspend.

- Fee increases may also be good reason to close a card, if you cannot convert the account to a lower or no-fee product.

- You may need to use old cards every so often to avoid fees or closures for inactivity. Any activity will do; there's no need for a large or additional expense.

-

3Open new lines of credit only when you need them. It’s fine to apply for a new credit card or loan occasionally. However, doing so constantly will make you look like more of a credit risk. Stick with your main credit cards and necessary loans like your mortgage or car payments. Avoid any new credit lines unless you need them.[21]

- It's usually best to avoid taking offers in stores for installment plans or store credit cards. These are additional, usually unnecessary lines of credit.

- Sometimes, opening a new card or credit line might be worthwhile. A card might have a great cashback offer or you might be able to save money by taking out an installment plan. Do your research to find good deals.

-

4Diversify your credit line if you have a thin credit history. Ironically, having too small of credit history is also bad for your credit score. This is called a thin file, and it means that you haven’t built up enough of a history for credit agencies to determine how reliable you are. Luckily, this is easy to fix with a few diversification tricks.[22]

- If you only have one credit card, try taking out a few different types of loans. For instance, you could take out a store installment plan on a piece of furniture instead of putting it on your card. Only do this if you can pay it back.

-

5Consider signing up for Experian Boost. This service considers other payments like your rent or utilities in determining your credit score. As long as you make payments reliably, participating should improve your score.

-

6Avoid cash-out refinancing. Refinancing your loans has a mixed effect on your credit score—sometimes it helps and sometimes it hurts. However, cash-out refinancing almost always hurts your score. This means that you take out a new loan against the existing equity. Adding another liability like this reduces your credit score.[23]

Assistance and Help

-

1Dispute items on your credit report that are incorrect. You will have better luck if you deal directly with the vendor who reported the incorrect information than depending on the credit bureaus to take your word for it. For example, if you paid off a car loan but the bank never reported it to the bureaus as paid, ask the bank to report the correction.

- For other types of reporting errors such as fraudulent use of your identity, provide all the forms of proof that you have to the bureaus, such as cancelled checks, stamped invoices, police reports, etc. Put everything in writing and follow up at least once per week by phone with the bureaus until the inaccuracies are corrected on your report.[24]

- Late payments showing on your credit report can really hurt your score. Collections, judgments and tax liens are devastating. You can try to negotiate with the entity that reported the collections, etc., for removal of such negative notations.

- Be persistent. If you have evidence and know that a charge is a mistake, the lender must remove it from your credit history by law, so don't let them give you the runaround.

- A credit counselor or advisor can help you dispute items on your credit report.[25]

-

2Contact lenders if you cannot make payments on time. If you experience a job loss or other misfortune, contact your lenders right away. The worst thing you can do is ignore them. Explain your financial situation and agree on a new payment schedule that you can manage. Get the agreement in writing and ask them to include a note that your payments will not be reported as late.

- It always helps to remind lenders that you've always been a good customer who pays bills on time. They're more willing to work with you if you have a good credit history.

- This is another good reason to keep your credit score in good shape. Lenders are less likely to work with you if you don't have a good credit history.

-

3Meet with a reputable credit counseling agency if you need financial advice to help get out of debt and improve your credit history. Find a find a low or zero cost agency to help you. There might be free services available from your employer, military base, credit union, housing authority, or a local branch of the U.S. Cooperative Extension.[26]

- A good financial adviser can also help you get your finances in order.

-

4Avoid credit repair businesses so you don't get scammed. You'll probably come across many offers online or in the mail about credit repair services. These companies claim that they can eliminate your debt and fix your credit score quickly. Many of these are scams that will not only fail to fix your credit score, but they might take your money too. Overall, these companies don't do anything that you can't do yourself to fix your credit.[27]

- Some major warning signs of a scam are demanding payment upfront, promising results, and telling you not to contact credit reporting agencies.[28]

- If you've been scammed by a company like this, report them to the Federal Trade Commission.

Expert Q&A

Did you know you can get expert answers for this article?

Unlock expert answers by supporting wikiHow

-

QuestionWhat should I do if I recently made a late payment on my credit card?

Derick VogelDerick Vogel is a Credit Expert and CEO of Credit Absolute, a credit counseling and educational company based in Scottsdale, Arizona. Derick has over 10 years of financial experience and specializes in consulting mortgages, loans, specializes in business credit, debt collections, financial budgeting, and student loan debt relief. He is a member of the National Association of Credit Services Organizations (NASCO) and is an Arizona Association of Mortgage Professional. He holds credit certificates from Dispute Suite in credit repair best practices and in Credit Repair Organizations Act (CROA) competency.

Derick VogelDerick Vogel is a Credit Expert and CEO of Credit Absolute, a credit counseling and educational company based in Scottsdale, Arizona. Derick has over 10 years of financial experience and specializes in consulting mortgages, loans, specializes in business credit, debt collections, financial budgeting, and student loan debt relief. He is a member of the National Association of Credit Services Organizations (NASCO) and is an Arizona Association of Mortgage Professional. He holds credit certificates from Dispute Suite in credit repair best practices and in Credit Repair Organizations Act (CROA) competency.

Credit Advisor & Owner, Credit AbsoluteYou should call the credit card company and let them know that it was an oversight and ask them to remove the late fee. Make sure you make the minimum payment—always make the minimum payment no matter what. Keep in mind that the creditor and credit bureaus are not allowed to report a 30-day late payment unless it's actually 30 days past the due date. If you made the payment 29 days after the due date, they still can't report a 30-day late payment. If they do, that could be a Fair Credit Reporting Act (FCRA) violation.

Support wikiHow by unlocking this expert answer.

-

QuestionWhat is the best way to dispute a credit report?Derick VogelDerick Vogel is a Credit Expert and CEO of Credit Absolute, a credit counseling and educational company based in Scottsdale, Arizona. Derick has over 10 years of financial experience and specializes in consulting mortgages, loans, specializes in business credit, debt collections, financial budgeting, and student loan debt relief. He is a member of the National Association of Credit Services Organizations (NASCO) and is an Arizona Association of Mortgage Professional. He holds credit certificates from Dispute Suite in credit repair best practices and in Credit Repair Organizations Act (CROA) competency.

Credit Advisor & Owner, Credit AbsoluteTalk to a credit counselor or advisor. They can help you dispute items on your credit report so it's accurate.Support wikiHow by unlocking this expert answer.

-

QuestionWhat is the optimal debt ratio?Derick VogelDerick Vogel is a Credit Expert and CEO of Credit Absolute, a credit counseling and educational company based in Scottsdale, Arizona. Derick has over 10 years of financial experience and specializes in consulting mortgages, loans, specializes in business credit, debt collections, financial budgeting, and student loan debt relief. He is a member of the National Association of Credit Services Organizations (NASCO) and is an Arizona Association of Mortgage Professional. He holds credit certificates from Dispute Suite in credit repair best practices and in Credit Repair Organizations Act (CROA) competency.

Credit Advisor & Owner, Credit AbsoluteKeeping your debt ratio under 30% will help you attain a good credit score. However, it's ideal to keep your debt ratio under 10% if you want a high credit score.Support wikiHow by unlocking this expert answer.

References

- ↑ http://www.consumerfinance.gov/askcfpb/319/how-does-my-credit-score-affect-my-ability-to-get-a-mortgage-loan.html

- ↑ http://www.investopedia.com/articles/pf/10/credit-score-factors.asp

- ↑ Derick Vogel. Credit Advisor & Owner, Credit Absolute. Expert Interview. 26 March 2020.

- ↑ http://www.consumerfinance.gov/askcfpb/319/how-does-my-credit-score-affect-my-ability-to-get-a-mortgage-loan.html

- ↑ https://www.myfico.com/credit-education/credit-scores/fico-score-versions

- ↑ https://www.myfico.com/credit-education/credit-scores/fico-score-versions

- ↑ http://www.creditinfocenter.com/creditreports/CreditBureauContactInfohtm.shtml

- ↑ http://www.myfico.com/CreditEducation/CreditScores.aspx

- ↑ Derick Vogel. Credit Advisor & Owner, Credit Absolute. Expert Interview. 26 March 2020.

- ↑ https://www.investopedia.com/how-to-improve-your-credit-score-4590097

- ↑ https://money.cnn.com/2018/03/29/pf/how-to-improve-credit-score/index.html

- ↑ Derick Vogel. Credit Advisor & Owner, Credit Absolute. Expert Interview. 26 March 2020.

- ↑ https://www.thebalance.com/improve-your-credit-score-960388

- ↑ https://www.federalreserve.gov/pubs/creditscore/creditscoretips_2.pdf

- ↑ Derick Vogel. Credit Advisor & Owner, Credit Absolute. Expert Interview. 26 March 2020.

- ↑ https://www.entrepreneur.com/article/168290

- ↑ https://www.thebalance.com/improve-your-credit-score-960388

- ↑ https://www.debt.org/credit/improving-your-score/

- ↑ https://www.cnbc.com/select/how-to-boost-your-credit-score-fast/

- ↑ https://www.debt.org/credit/improving-your-score/

- ↑ https://www.entrepreneur.com/article/168290

- ↑ https://www.investopedia.com/how-to-improve-your-credit-score-4590097

- ↑ https://www.investopedia.com/mortgage/refinance/my-fico-score/

- ↑ https://www.annualcreditreport.com/index.action

- ↑ Derick Vogel. Credit Advisor & Owner, Credit Absolute. Expert Interview. 26 March 2020.

- ↑ http://www.justice.gov/ust/list-credit-counseling-agencies-approved-pursuant-11-usc-111

- ↑ https://www.federalreserve.gov/pubs/creditscore/creditscoretips_2.pdf

- ↑ https://www.consumerfinance.gov/ask-cfpb/how-can-i-tell-a-credit-repair-scam-from-a-reputable-credit-counselor-en-1343/

- ↑ https://www.nerdwallet.com/article/finance/credit-score-does-carrying-a-balance-help

About This Article

To improve your credit score, try to pay off as much of your debt as possible, which will help your credit score go up. Also, build up different types of credit, like a credit card, a car payment, or a mortgage, since you'll have a higher score if you diversify your lines of credit. You should also make sure you're paying all of your bills on time since late payments will lower your score. For more advice from our Financial co-author, like how to interpret your current credit report, read on!