This article was written by Jennifer Mueller, JD. Jennifer Mueller is an in-house legal expert at wikiHow. Jennifer reviews, fact-checks, and evaluates wikiHow's legal content to ensure thoroughness and accuracy. She received her JD from Indiana University Maurer School of Law in 2006.

This article has been viewed 21,923 times.

Although it may not be the most exciting thing you do, an annual operating budget is essential for every business, whether for-profit company, non-profit organization, or professional partnership. Your operating budget is a valuable tool that can help your business succeed by giving you an in-depth understanding of where your money is going and where you have room to grow. To determine your operating budget, you must itemize your business's expenses and accurately predict annual income and cash flow.[1] [2]

Steps

Itemizing Expenses

-

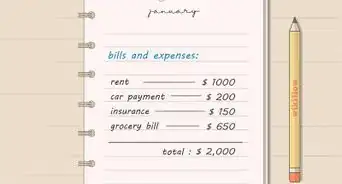

1Gather your monthly bills. Your first step in determining an operating budget is calculating the amount of regular payments your business makes for rent, utilities, and other such expenses that are required each month regardless of your business's income.[3] [4]

- These are fixed costs that your business will incur regardless of your profit. Think of similar bills that you have in your personal life, such as your housing payment, electricity, and telephone.

- Don't forget any monthly fees you pay for phone or internet service, as well as hosting fees for your business's website, or professional fees to an accountant or tax professional.

- You may want to prioritize these expenses, particularly if your business is a start-up or your performance is untested.

- Consider which of these things your business could do without if finances were tight. Any additional fees to break a contract should factor into these calculations.

- At the same time, you want to make sure you have enough room in your budget to accommodate any fluctuations in these expenses. For example, your utility bills may be higher than average in the summer months if your business is located in a hot climate.

- Keep in mind that generally speaking a strong budget will over-estimate expenses and under-estimate profits.

-

2Calculate your payroll. Your payroll also is a non-discretionary expense that includes not only the amounts you pay each employee, but also payments for workers' compensation, unemployment, taxes, and other benefits.[5] [6]

- If you use an accountant or tax professional, you may need to work with them to ensure that you're accurately calculating the cost of payroll taxes and other expenses.

- Be sure to include pay raises if you've created a regular performance review system, as well as any potential payments for bonuses.

- This portion of your budget should focus exclusively on employees on your payroll – not any independent contractors who you may hire for temporary jobs or to perform discrete tasks.

- Make sure you're leaving enough room in your payroll budget to expand throughout the year if need be. For example, if you own a retail store and know that you probably will need to hire a couple of additional sales workers during the holiday season, their pay should be included.

Advertisement -

3Include taxes, insurance premiums, and licensing fees. Taxes, insurance premiums, and licensing fees are essential for your business to operate legally and therefore must be included as regular expenses in your budget.[7] [8]

- These amounts typically will vary depending on the type of business you're running and where that business is located.

- Typically you will have premiums for liability insurance, as well as auto insurance for any vehicles that are used in your business for deliveries or other purposes.

- Professional companies also typically must pay premiums for malpractice insurance.

- If you're just starting your business, your business plan should include a section that details the licenses and inspections you need to open your doors for the first time. These amounts should be included in your budget.

- Also make sure you're planning for contingencies. If your business fails an inspection, your budget may not necessarily include costs for replacing or repairing items that weren't up to standard, but it should include any additional fees you may have to pay.

- Include in this portion of your budget any corporate dues or registration fees that your state requires, depending on how your business is organized.

-

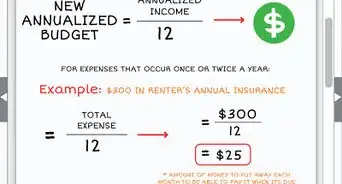

4Consider budgeting for one-time purchases. Particularly if your business is a start-up, you must account for expenses on equipment and supplies that aren't necessarily ongoing expenses but are things that must be purchased for your business to operate effectively.[9]

- Although not necessarily a one-time expense, you also must consider any expenses for building and maintaining inventory.

- If you are just starting your business, you may have to spend more initially for a start-up inventory than you would spend to maintain a working inventory sufficient for normal operations.

- If you work with a tax professional, speak with them regarding whether certain one-time expenses can be deducted from your business's taxes all at once, or must be depreciated over time. Tax-deductible expenses and depreciation should be factored into your budget.

Predicting Income

-

1Review past income reports. If your business has already been in operation for a year or more, you have an easier job of predicting future income, because you can rely on income you've recorded in previous years.[10] [11]

- Pay attention to any changes that have occurred in your business since the report was issued and conservatively account for those changes.

- For example, if last year's income report covered two locations, and you have since opened two more locations, that doesn't necessarily mean you should predict your income will double.

- Rather, if you've expanded by opening new locations, you should predict income from those new locations based on the income your established locations brought in during their first year.

- Account for growth, but be careful not to overestimate or be too optimistic. Just as you built in larger sums of money for expenses than your past experience might dictate, you also want to be very conservative about your income predictions.

- Try to focus as much as possible on income that's nearly guaranteed. For example, if you have clients under contract, you can conservatively count on the income that is assured by those contracts.

-

2Research your industry and target market. If you're starting a new business, predicting income may be more difficult. You must thoroughly research your industry, including key competitors, and your target customer base.[12] [13]

- Owners of start-ups effectively must create a budget from scratch, without being able to draw upon past experience. You may want to talk to business owners with similar operations to get ideas on what to expect.

- You likely already have created a business plan with some projections and estimates, particularly if you sought investors. That business plan and the research you did to complete it can serve as a guide.

- You also want to look at industry benchmarks and statistics to find out what level of income you can safely predict for your business.

- Keep in mind that your income predictions will fluctuate depending on the kind of competition you're experiencing in your area. If there are a lot of direct competitors nearby, you may have a hard time achieving profitability in your first few years.

-

3Create a cash flow budget. No amount of income is sufficient if it doesn't provide your business with enough cash flow to pay your bills on time. Estimating cash flow requires not just an understanding of how much income you'll produce, but when that income will be realized.[14] [15]

- Look at your budget on a monthly basis to determine when your bills are due and when you can expect to receive income.

- If you're billing clients, factor in the time they have to pay after they receive an invoice. If you give clients 30 days from the date of receipt to pay their invoice, that income shouldn't be included in your cash flow budget until the 30th day.

- If you have a retail business, you may want to estimate your daily or weekly sales, and create sales goals for your team that will enable you to make budget and cover the business's expenses.

- For ease of budgeting, consider tying bonuses to the percentage that actual sales exceed your sales goals.

Playing with Variables

-

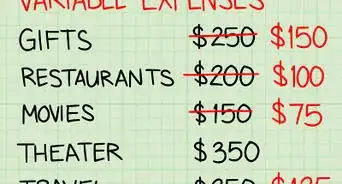

1Plug in several alternatives. Since there are many events or situations that could effect your business's income and expenses, you want your budget to be able to compensate for changes you might have to make over the course of the year.[16] [17]

- Consider scenarios that are likely to happen, or that are common in your industry. For example, if you have a retail store, you want to account for a significant slump in sales in the winter months following the holiday boom.

- If your business is in a seasonal industry such as construction, you can use different alternatives to help budget your income for lean months and ensure you can meet payroll when new projects start so your business can take on more clients.

- Alternatives can illustrate the flexibility of your budget to handle different scenarios without endangering your business's finances.

- These evaluations also can point out vulnerabilities where you need to budget more money to offset potential risk.

-

2Create hypotheticals. Evaluating your budget under a number of "what if" situations that reflect potential risks in your industry can test the budget's resiliency and flexibility, enabling you to produce a stronger operating budget.[18] [19]

- You want to see how your budget performs in the face of common calamities in your industry, but you also may want to evaluate less probable scenarios.

- If your business is unable to quickly recover after a catastrophe, you may want to consider having more money in reserve that you can tap in an emergency.

-

3Factor in different growth rates. Try using at least three growth rates – one optimistic, one conservative or realistic, and one pessimistic – to examine your income predictions and evaluate how your budget performs.[20] [21]

- Your best-case scenario allows you to brainstorm additional projects or improvements you can undertake if your business exceeds expectations.

- Keep in mind that you want your profit to work for you, not simply sit in a bank account and gather dust. Your business will be more financially healthy if you have the ability to quickly re-invest in facilities and operations when you're performing well.

- Evaluating the business's financial fitness in a worst-case scenario allows you to create proactive plans to keep your business on track should disaster strike. Ultimately this preparation can take some stress out of owning and operating a small business.

-

4Review your budget often. Once you've completed your budget, you should compare it to your business's actual income and expenses at least once a quarter and make adjustments where necessary. This ensures your budget is an accurate and realistic reflection of your business's financial picture.[22] [23]

- If you have a start-up business, and your budget is based mostly on guess work, review your budget more frequently.

- Going over the numbers once a month will ensure that you know how your business is really doing and have the ability to quickly adjust your expenses or income predictions where necessary so that your budget continues to be useful.

- For a more established business, you may find that you don't need to go over the budget more than once a quarter. Regardless, adjusting your budget to correspond to the facts on the ground can turn it into a strong and effective tool for plotting your business's growth.

References

- ↑ http://www.inc.com/guides/2010/10/how-to-set-an-annual-budget.html

- ↑ https://www.entrepreneur.com/article/21942

- ↑ http://www.inc.com/guides/2010/10/how-to-set-an-annual-budget.html

- ↑ https://www.score.org/blog/2015/hal-shelton/how-set-and-maintain-budget-your-small-business

- ↑ http://www.inc.com/guides/2010/10/how-to-set-an-annual-budget.html

- ↑ https://www.score.org/blog/2015/hal-shelton/how-set-and-maintain-budget-your-small-business

- ↑ http://www.inc.com/guides/2010/10/how-to-set-an-annual-budget.html

- ↑ https://www.score.org/blog/2015/hal-shelton/how-set-and-maintain-budget-your-small-business

- ↑ https://www.entrepreneur.com/article/21942

- ↑ http://www.inc.com/guides/2010/10/how-to-set-an-annual-budget.html

- ↑ http://smallbusiness.intuit.com/news/Achieving-sales-&-profitability/19283950/Creating-a-Budget-for-Your-Small-Business:-The-Basics.jsp

- ↑ http://www.inc.com/guides/2010/10/how-to-set-an-annual-budget.html

- ↑ http://smallbusiness.intuit.com/news/Achieving-sales-&-profitability/19283950/Creating-a-Budget-for-Your-Small-Business:-The-Basics.jsp

- ↑ http://www.inc.com/guides/2010/10/how-to-set-an-annual-budget.html

- ↑ http://smallbusiness.intuit.com/news/Achieving-sales-&-profitability/19283950/Creating-a-Budget-for-Your-Small-Business:-The-Basics.jsp

- ↑ http://www.nonprofitaccountingbasics.org/reporting-operations/budgeting-terms-concepts

- ↑ https://www.sba.gov/blogs/how-build-and-use-business-budget-thats-useful-all-year-long

- ↑ http://www.nonprofitaccountingbasics.org/reporting-operations/budgeting-terms-concepts

- ↑ https://www.sba.gov/blogs/how-build-and-use-business-budget-thats-useful-all-year-long

- ↑ http://www.nonprofitaccountingbasics.org/reporting-operations/budgeting-terms-concepts

- ↑ https://www.sba.gov/blogs/how-build-and-use-business-budget-thats-useful-all-year-long

- ↑ http://www.inc.com/guides/2010/10/how-to-set-an-annual-budget.html

- ↑ https://www.sba.gov/blogs/how-build-and-use-business-budget-thats-useful-all-year-long

About This Article