This article was co-authored by Michael R. Lewis. Michael R. Lewis is a retired corporate executive, entrepreneur, and investment advisor in Texas. He has over 40 years of experience in business and finance, including as a Vice President for Blue Cross Blue Shield of Texas. He has a BBA in Industrial Management from the University of Texas at Austin.

This article has been viewed 132,994 times.

Identifying the average operating assets or AOA associated with a company during a specific accounting period is very important to the business process. This type of calculation makes it easier to determine if the business is making efficient use of its resources in order to generate revenue. Fortunately, the process used in calculating AOA is very simple, making it easy to manage the calculation with relatively little effort.

Steps

Calculating Average Operating Assets

-

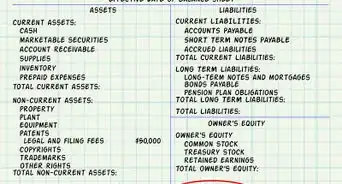

1Identify the assets that are considered part of the operating process. This typically includes assets such as fixed assets, the accounts receivable currently outstanding, equipment, the balance of cash accounts, and the total inventory that is currently on hand as of the last date of the period under consideration. Do not include assets that are not part of the operating (production) process.[1]

- Include some intangible assets if they are necessary to the business, such as licenses and patents.

- You would also include land and equipment, unless the equipment is idle.

-

2Calculate the total monetary value of the beginning operating assets. This total is the total operating assets on hand as of the first day of the time period under consideration. For example, if the calculation is based on finding the average operating expenses for a quarter, the beginning assets will be those on hand as of the first day of that quarter.

- You can determine the monetary value of the inventory and equipment, as well as the cash balance and outstanding accounts receivables, by looking in the General Ledger and relevant accounts.

- For this example, the value of beginning operating assets is $500,000 on April 1.

Advertisement -

3Determine the total monetary value of the ending operating assets. These are the assets on hand at the end of the period under consideration. This figure is usually referred to as the ending assets and will be different from the figure identified for the beginning of the period. This is because some of the assets will be consumed in the interim, while other assets are acquired during that same time frame.

- When calculating ending assets for a given quarter, use the total value of assets as of the last business day of that quarter. For this example, the value of the ending operating assets is $550,000 on June 30 (a one-quarter time period).

-

4Add the total amount of beginning assets to the total amount of the ending assets. Combining the two figures makes it possible to arrive at a number that can then be used to identify the average operating assets for the desired time period. You will be taking an average of the two numbers.

- $500,000 beginning operating assets + $550,000 ending operating assets = $1,050,000.

-

5Divide the combined amount of beginning and ending assets by 2. The result will be the average operating assets for that period, providing a figure that can easily be compared to the AOA for previous periods. This in turn makes it easier to determine if the company is becoming more efficient in the use of its resources or if a negative trend is emerging that needs to be addressed.

- For example, divide $1,050,000 by 2 = $525,000. Compare this to previous quarters' numbers. If it is higher look into reducing accounts receivable levels or reducing inventory.

Calculating Operating Assets Ratio

-

1Calculate and compare an operating assets ratio. An operating assets ratio is the operating assets divided by total assets less cash It is used to analyze which company assets are not contributing to revenue and can therefore be reduced or eliminated. The formula is: operating assets/total non-cash assets.

-

2Add up operating assets. These include inventory, accounts receivable, fixtures and production equipment. Be sure to also include all non-production equipment, obsolete inventory and overdue accounts receivable. Note that cash will not be used in this calculation.

- For example, $85,000 inventory + $50,000 accounts receivable + $10,000 fixtures + $70,000 production equipment + $120,000 non-production equipment + $90,000 obsolete inventory + $75,000 overdue account receivable = $500,000 total operating assets.

-

3Use the operating assets ratio. Divide $215,000 by $500,000 = .43 operating assets ratio. Compare this to the ratio of competitors that you can find on their balance sheet published on their website. The lower the ratio the better.

- This example identifies $285,000 of non-revenue generating assets that could be reduced or eliminated and converted into cash. Obsolete inventory and non-production equipment could be sold and overdue accounts receivable could be written off.

Using Average Operating Assets Data

-

1Calculate Return on Investment (ROI). Knowing the average operating assets numbers for a given period can be used with other financial data to analyze the health of the business.

- ROI is calculated by taking the net profit of the company divided by its average operating assets. For example, $100,000 (net profit) /$525,000 (average operating assets) = 19.0%.

-

2Calculate asset turnover. Asset turnover is the ratio of a company’s sales compared to the value of its average operating assets. This ratio can be an indicator of the efficiency with which a company is using its assets in generating revenue. The formula is Sales or Revenues / Total Assets = Asset Turnover.

- For example, $100,000 sales / $80,000 assets = 1.25. The higher the ratio the better a company is utilizing its assets.

- This ratio can be used to compare productivity between companies within the same industry. A higher asset turnover ratio is preferred.

- It can also be used to measure productivity increases or decreases over time within the same company.[2]

-

3Keep good records. You will want to save all invoices of operating assets purchased from vendors in order to accurately calculate the beginning and ending values. These will also be required for future audits so should be saved for seven years.

References

About This Article