This article was co-authored by Ara Oghoorian, CPA. Ara Oghoorian is a Certified Financial Accountant (CFA), Certified Financial Planner (CFP), a Certified Public Accountant (CPA), and the Founder of ACap Advisors & Accountants, a boutique wealth management and full-service accounting firm based in Los Angeles, California. With over 26 years of experience in the financial industry, Ara founded ACap Asset Management in 2009. He has previously worked with the Federal Reserve Bank of San Francisco, the U.S. Department of the Treasury, and the Ministry of Finance and Economy in the Republic of Armenia. Ara has a BS in Accounting and Finance from San Francisco State University, is a Commissioned Bank Examiner through the Federal Reserve Board of Governors, holds the Chartered Financial Analyst designation, is a Certified Financial Planner™ practitioner, has a Certified Public Accountant license, is an Enrolled Agent, and holds the Series 65 license.

There are 14 references cited in this article, which can be found at the bottom of the page.

wikiHow marks an article as reader-approved once it receives enough positive feedback. This article has 23 testimonials from our readers, earning it our reader-approved status.

This article has been viewed 512,062 times.

Accounting, a meticulous recording of financial transactions, is a crucial process required for the success of businesses both big and small. While large businesses will usually employ a sizable accounting department with many employees (as well as doing business with a separate auditing firm), smaller businesses may employ only a bookkeeper. In a single-person business, the business owner may need to handle the accounting themselves, without the help of a bookkeeper. Whether you're trying to manage your own finances or are interested in finding work as a bookkeeper for another person's business, learning the basics of accounting can help get you started.

Steps

Developing Stronger Accounting Skills

-

1Understand the difference between bookkeeping and accounting. Bookkeeping and accounting are terms often used interchangeably. However, the skills and responsibilities required of each are somewhat different. Bookkeepers generally keep records of sales and record them in the books directly. They do the day-to-day work of making sure every dollar the business makes and spends gets recorded. An accountant, on the other hand, creates and analyzes financial statements, and can also audit the business's books to ensure accuracy and proper reporting.

- Bookkeepers and Accountants may works in tandem to provide a full level of service to a business.

- In many cases, the distinction between the two is formalized by a professional degree, state certification, or industry organization.[1]

-

2Become familiar with creating spreadsheets. Microsoft Excel or other spreadsheet software are invaluable to accountants, as they help you track numbers in a graph or conduct calculations to create a finance spreadsheet. Even if you know the basics, you can always brush up and learn intermediate or advanced skills for creating spreadsheets, charts, and graphs.Advertisement

-

3Read books on accounting. Visit your local library to find books on accounting, or purchase a book from the bookseller of your choice. Look for entry-level books written by authors who have experience in accounting, as these books will be more likely to contain researched information.

- Introduction to Accounting, by Pru Marriott, JR Edwards, and Howard J Mellett, is a widely used introductory textbook that is considered an excellent primer for both general education purposes as well as for learners who intend to specialize in accounting.[2]

- College Accounting: A Career Approach by Cathy J. Scott is a widely used college textbook for accounting and financial management courses. The book also has the option of coming with a Quickbooks Accounting CD-ROM that can be invaluable for aspiring accountants.

- Financial Statements: A Step-by-Step Guide to Understanding and Creating Financial Reports by Thomas R. Ittelson is a best-selling introduction to financial reports, and may be a good first step for learners interested in entering the field of accounting.

-

4Take an accounting course. You can always look into courses at your local community college, or take online courses in accounting for free. Try websites like Coursera or other online education platforms to find free courses taught by distinguished professionals in the field of accounting.

- Not everything needed to be a great accountant can be learned in a course.

Practicing Accounting Basics

-

1Understand dual-entry bookkeeping. Accountants make two or more entries for each transaction recorded by the business. These can be thought of as an increase in one or more accounts and an identical decrease in one or more other accounts. For example, a payment made for a sale previously made on credit would result in an increase in the cash account and a decrease in Accounts Receivable (money owed to the business by customers who have purchased items on credit but not yet paid). These entries would be made for the same amount (the amount of the sale).[3]

-

2Practice recording debits and credits. When dual-entry records are made, they are done in the form of debits and credits. These represent whether or not certain accounts are increased or decreased by a transaction. Using them is relatively if you remember two things:

- Debit means the record goes in the left side of the t-account and credit means you should use the right side. This refers to a standard t-account journal in which records are made on either side of the vertical portion of the "T".

- Assets=Liabilities+Owner's Equity. This is the accounting equation. Memorize this above all else. It works as a sort of guide to debits and credits. For the portion left of the "=," debits increase the account and credits decrease it. For the right side, the opposite is true.

- This means that when asset accounts, like cash, are debited, they are increased. However, when liability accounts, like accounts payable, are debited, they decrease.[4]

- Practice by working out how you would enter different common transactions, like paying your electric bill or receiving a cash payment from a customer.

-

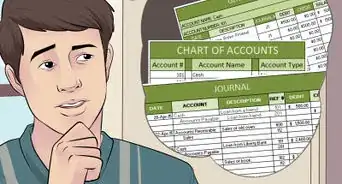

3Set up and maintain a general ledger. The general ledger is where the dual-entry transaction are recorded. Each individual record (the various debits and credits in the transaction) is made in the relevant account within the ledger. So, for a cash bill payment, an entry would be made in the cash account and another, separate entry made in the accrued expenses account. This process is greatly simplified when you use accounting software, but can also be done by hand relatively simply.[5]

-

4Distinguish between cash and accruals. A cash transaction is the type of trade that occurs when a customer buys a pack of gum from the store and you receive the payment on the spot, and then give them the gum in exchange. Accruals, on the other hand, take into account things like credit, invoices, and billing, rather than direct payment at the time of business, as well intangible assets like goodwill.[6]

Learning Financial Statements

-

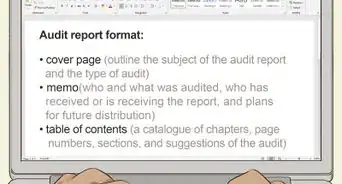

1Know how financial statements are created. Financial statements reflect the current financial health of the business and its financial performance over the last accounting period. The financial statements are created from the information contained within the general ledger. At the end of the accounting period, each account is totaled up to create a trial balance. The total debits and credits in all accounts should be equal. If they are not, the accountant must re-check the balances of each account and make adjustments or corrections where necessary.

- When the accounts are adjusted and correct, the accountant can enter summaries of the information contained in them into the financial statements.[7]

- As you study financial statements, you should aim to be able to create them on your own and be able to identify what all of the numbers on a certain statement mean.[8]

-

2Learn how to create an income statement. An income statement is the most basic principle of accounting. It records a company's profit margins over a specified duration of time, ranging anywhere from one week to one year. The income statement is determined by two factors: the business's revenues and its expenses.[9]

- Revenue is the inflow of cash in exchange for goods and services earned over time —though not necessarily the money actually paid to the company over that period of time. Revenue may include cash transactions as well as accruals. If accruals are included in the income statement, then the revenue of a given week or month takes into account the invoices and bills that were sent out during that time, even if the money will not be collected until the next income statement's period. Income statements are therefore intended to show how profitable a business was during that recorded period of time, not necessarily how much money a business took in during that time.[10]

- Expenses are any use of money to the company, whether due to the cost of materials and supplies or labor/wages. Much like revenues, expenses are reported during the period of time in which those expenses were incurred, not necessarily when the company paid for those expenses.[11]

- The matching principle of accounting requires a company to match related expenses and revenues together whenever possible in order to ascertain a company's actual profitability over the course of a given time period. In a successful business this should more or less result in a cause-and-effect relationship, where, for example, increased sales will increase the company's revenue while also resulting in business-related expenses: an increased need to buy more supplies for the store and an increase in expenses for sales commissions, if applicable.[12]

-

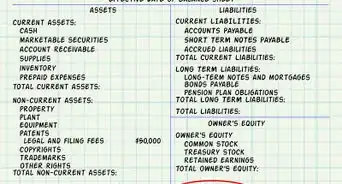

3Create a balance sheet. Unlike an income statement, which deals with a period of time, a balance sheet can be thought of as essentially a snapshot of your business at one particular point in time.[13] A balance sheet has three important components: the business's assets, liabilities, and the stockholder's or owner's equity at a given point in time.[14] It may be helpful to think of the balance equation in terms of a company's assets being equal to the company's liabilities plus the owner's/shareholder's equity. In other words, what you have is always determined by what you owe plus what is currently yours to keep.[15]

- Assets are what a company owns. It may be helpful to think of assets as all of the resources a company has at its disposal: namely, the vehicles, cash, supplies, and equipment a company owns at that given point in time.[16] Assets can be tangible (a plant, equipment) and intangible (patents, trademarks, goodwill).

- Liabilities are any amount that is owed to others at the time of the balance sheet's creation. Liabilities can include loans that must be paid back, any money that is owed for supplies given on credit, and any wages owed to employees that have not yet been paid.[17]

- Equity is the difference between the assets and the liabilities. Equity is sometimes thought of as the "book value" of a company or business.[18] If the company is a large corporation, the equity may belong to stockholders; if the business is owned by one single person, then the equity is an Owner's Equity.[19]

-

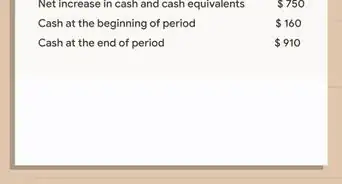

4Generate a statement of cash flows. Essentially, a cash flows statement specifies how cash has been generated and used by a business, as well as that business' investing and financing activities, over a specified period of time. The statement of cash flows is mostly derived from a business's balance sheets and income statements for that same time period.[20]

Learning the Principles of Accounting

-

1Follow the generally accepted accounting principles (GAAP). The basic principles that guide accounting practices rely on a set of principles and assumptions designed to guarantee transparency and integrity in all business transactions.

- The Economic Entity Assumption is the requirement that an accountant working for a sole proprietorship (a business where a single person owns the company) must maintain a separate ledger for business transactions that does not include the business owner's personal expenses or transactions.[21]

- The Monetary Unit Assumption is the agreement that economic activity, at least in the United States, will be measured in US currency, and therefore only activity that can be translated into US currency will be recorded.[22]

- The Time Period Assumption is the agreement that all business transactions will be represented in distinct time intervals, and that those intervals will be recorded accurately. These intervals are typically relatively short: at the very least an annual report is made, though reports are often made at weekly intervals in many companies. The report must also specify when that time interval began and ended. In other words, it's not enough to include the date of the report; an accountant must clarify in that report whether the report corresponds to one week, one month, one financial quarter, or one year.[23]

- The Cost Principle refers to the amount of money spent at the time of a given transaction, without taking inflation into account.[24]

- The Full Disclosure Principle requires accountants to disclose relevant financial information to any interested parties, particularly investors and lenders. This information must be disclosed either in the body of a financial statement, or in the notes at the end of that statement.[25]

- The Going Concern Principle assumes that the company will remain in operation for the foreseeable future, and requires the accountant to disclose any information regarding the compromised future or certain failure of a company. In other words, if an accountant believes the company will go bankrupt in the foreseeable future, he is obligated to disclose that information to investors and any other interested parties.[26]

- The Matching Principle mandates that expenses be paired with revenues in all financial reports.[27]

- The Revenue Recognition Principle is an agreement that revenue will be recorded as having occurred at the time the transaction is completed, not when the money is actually paid to the business.[28]

- Materiality is a guideline which grants accountants some degree of professional judgment in determining whether or not a given amount is insignificant to the report. This does not mean an accountant may report inaccurately; rather, it addresses an accountant's decision to round to the nearest dollar, for example, in reporting on a business's financial transactions.[29]

- Conservatism is a principle that advises that an accountant may report potential losses for a business (in fact, he has an obligation to report such losses), but he may not report potential gains as actual gains. This is to prevent investors from having an inaccurate picture of the company's financial situation.[30]

-

2Follow the rules and standards of the Financial Accounting Standards Board. The Financial Accounting Standards Board (FASB) has laid out extensive rules and standards which ultimately seek to ensure that interested parties have reliable, accurate information, and that accountants work ethically and report honestly. A detailed layout of the FASB's conceptual framework can be found on the FASB website.

-

3Follow the generally accepted industry practices. These are expectations that working accountants have of other accountants, which help guide the industry. They include:

- Reliability, verifiability, and objectivity principles require accountants to report on numbers that other accountants would agree on. This is both for the professional dignity of the accountant and to ensure that any future transactions are fair and honest.[31]

- Consistency requires an account to be consistent in how he applies various practices and procedures to a financial report. If, for example, a business changes its cost flow assumption, the accountant for that business has an obligation to report on that change.[32]

- Comparability requires accountants to conform to certain standards, such as the generally accepted accounting principles (GAAP), to ensure that one company's financial reports can be easily compared to another company's financial reports.[33]

How Do You Calculate Retained Earnings?

Expert Q&A

Did you know you can get expert answers for this article?

Unlock expert answers by supporting wikiHow

-

QuestionWhat do I need to be a good accountant?

Ara Oghoorian, CPAAra Oghoorian is a Certified Financial Accountant (CFA), Certified Financial Planner (CFP), a Certified Public Accountant (CPA), and the Founder of ACap Advisors & Accountants, a boutique wealth management and full-service accounting firm based in Los Angeles, California. With over 26 years of experience in the financial industry, Ara founded ACap Asset Management in 2009. He has previously worked with the Federal Reserve Bank of San Francisco, the U.S. Department of the Treasury, and the Ministry of Finance and Economy in the Republic of Armenia. Ara has a BS in Accounting and Finance from San Francisco State University, is a Commissioned Bank Examiner through the Federal Reserve Board of Governors, holds the Chartered Financial Analyst designation, is a Certified Financial Planner™ practitioner, has a Certified Public Accountant license, is an Enrolled Agent, and holds the Series 65 license.

Ara Oghoorian, CPAAra Oghoorian is a Certified Financial Accountant (CFA), Certified Financial Planner (CFP), a Certified Public Accountant (CPA), and the Founder of ACap Advisors & Accountants, a boutique wealth management and full-service accounting firm based in Los Angeles, California. With over 26 years of experience in the financial industry, Ara founded ACap Asset Management in 2009. He has previously worked with the Federal Reserve Bank of San Francisco, the U.S. Department of the Treasury, and the Ministry of Finance and Economy in the Republic of Armenia. Ara has a BS in Accounting and Finance from San Francisco State University, is a Commissioned Bank Examiner through the Federal Reserve Board of Governors, holds the Chartered Financial Analyst designation, is a Certified Financial Planner™ practitioner, has a Certified Public Accountant license, is an Enrolled Agent, and holds the Series 65 license.

Certified Financial Planner & AccountantStrong analytical and problem-solving skills are important so you can develop financial statements, understand numbers, and make predictions from those financial statements. However, good interpersonal skills are also essential for when you work on teams.

Support wikiHow by unlocking this expert answer.

-

QuestionCan you do accounting by yourself with software?Ara Oghoorian, CPAAra Oghoorian is a Certified Financial Accountant (CFA), Certified Financial Planner (CFP), a Certified Public Accountant (CPA), and the Founder of ACap Advisors & Accountants, a boutique wealth management and full-service accounting firm based in Los Angeles, California. With over 26 years of experience in the financial industry, Ara founded ACap Asset Management in 2009. He has previously worked with the Federal Reserve Bank of San Francisco, the U.S. Department of the Treasury, and the Ministry of Finance and Economy in the Republic of Armenia. Ara has a BS in Accounting and Finance from San Francisco State University, is a Commissioned Bank Examiner through the Federal Reserve Board of Governors, holds the Chartered Financial Analyst designation, is a Certified Financial Planner™ practitioner, has a Certified Public Accountant license, is an Enrolled Agent, and holds the Series 65 license.

Certified Financial Planner & AccountantYes, but ne careful not to rely too much on your software to do your back-end journal entries, because if you don't understand the journal entry behind a mistake it's difficult to fix. Anytime anything goes on a financial statement, there has to be a journal entry.Support wikiHow by unlocking this expert answer.

References

- ↑ http://quickbooks.intuit.com/r/bookkeeping/whats-the-difference-between-a-bookkeeper-and-an-accountant/

- ↑ http://trove.nla.gov.au/work/16405389?selectedversion=NBD22975854

- ↑ http://www.accountingcoach.com/accounting-basics/explanation/5

- ↑ http://www.accountingcoach.com/accounting-basics/explanation/5

- ↑ http://www.investopedia.com/terms/g/generalledger.asp?layout=orig

- ↑ http://www.investopedia.com/university/accounting/accounting3.asp

- ↑ http://www.investopedia.com/university/accounting/accounting4.asp

- ↑ Ara Oghoorian, CPA. Certified Public Accountant. Expert Interview. 11 March 2020.

- ↑ http://www.accountingcoach.com/accounting-basics/explanation/2

- ↑ http://www.accountingcoach.com/accounting-basics/explanation/2

- ↑ http://www.accountingcoach.com/accounting-basics/explanation/2

- ↑ http://www.accountingcoach.com/accounting-basics/explanation/2

- ↑ https://www.sba.gov/sites/default/files/Introduction%20to%20Accounting_Transcript_0.pdf

- ↑ http://www.accountingcoach.com/accounting-basics/explanation/3

- ↑ https://www.sba.gov/sites/default/files/Introduction%20to%20Accounting_Transcript_0.pdf

- ↑ http://www.accountingcoach.com/accounting-basics/explanation/3

- ↑ http://www.accountingcoach.com/accounting-basics/explanation/4

- ↑ http://www.accountingcoach.com/accounting-basics/explanation/4

- ↑ http://www.accountingcoach.com/accounting-basics/explanation/4

- ↑ http://www.accountingcoach.com/accounting-basics/explanation/5

- ↑ http://www.accountingcoach.com/accounting-principles/explanation

- ↑ http://www.accountingcoach.com/accounting-principles/explanation

- ↑ http://www.accountingcoach.com/accounting-principles/explanation

- ↑ http://www.accountingcoach.com/accounting-principles/explanation

- ↑ http://www.accountingcoach.com/accounting-principles/explanation

- ↑ http://www.accountingcoach.com/accounting-principles/explanation

- ↑ http://www.accountingcoach.com/accounting-principles/explanation

- ↑ http://www.accountingcoach.com/accounting-principles/explanation

- ↑ http://www.accountingcoach.com/accounting-principles/explanation

- ↑ http://www.accountingcoach.com/accounting-principles/explanation

- ↑ http://www.accountingcoach.com/accounting-principles/explanation/2

- ↑ http://www.accountingcoach.com/accounting-principles/explanation/2

- ↑ http://www.accountingcoach.com/accounting-principles/explanation/2

- ↑ http://www.calcpa.org/cpa-career-center/cpa-requirements

About This Article

To learn accounting on your own, start by reading books on the subject and familiarizing yourself with how to create finance spreadsheets. Practice basic accounting skills like recording debits and credits and setting up and maintaining ledgers. Be sure to follow generally accepted accounting principles, as well as the rules and standards set by the Financial Accounting Standards Board! To learn more details about financial statements, read on!