This article was co-authored by Clinton M. Sandvick, JD, PhD. Clinton M. Sandvick worked as a civil litigator in California for over 7 years. He received his JD from the University of Wisconsin-Madison in 1998 and his PhD in American History from the University of Oregon in 2013.

There are 18 references cited in this article, which can be found at the bottom of the page.

This article has been viewed 19,617 times.

If you are an employer who has one or more employees, you will most likely be required to withhold various taxes from every employee's paycheck. To set up your withholding procedures, you will need to apply for tax identification numbers with your state department of revenue and the Internal Revenue Service (IRS). When it comes time to withhold taxes, you will generally withhold state and federal income tax as well as federal social security and Medicare taxes. You may also be required to withhold other taxes periodically (e.g., supplemental payments). In addition to withholding funds from every employee's paycheck, you are also required to deposit those funds with your state and federal government periodically. Finally, either quarterly or once a year, you will be required to file a return as an employer.

Steps

Registering Your Business

-

1Apply for required identification numbers. When you start a business and plan on having employees, you must register with your state and federal government in order to obtain employer identification numbers. The federal identification number you will need is called a "federal employer identification number" (FEIN). It will be a nine-digit number assigned to you by the IRS and will be used when you report withholding. Each state will have its own tax ID number you will need as well. For example, in Minnesota, you will need to apply for a number from the Department of Revenue.

- To register for a FEIN, apply online with the IRS. The form you will use is SS-4.[1]

- Call your state department of revenue to get information about applying for your state tax ID number.

- If you fail to obtain these identification numbers, you may be assessed fines when you report withholding information.[2]

-

2Verify every employee's eligibility to work. Every employee you hire must be legally eligible to work in the United States. If you are unable to verify this information, hire them, and withhold taxes from them, you may be assessed penalties by the IRS. To verify every employee's eligibility to work, ask each one to fill out Form I-9, which is available on the U.S. Citizenship and Immigration Services website.[3]

- Once each employee fills out Form I-9, you are required to keep it on file for a period of three years. If the IRS requests a copy, you are required to furnish one.[4]

Advertisement -

3Confirm each employee's Social Security number. Each employee you hire should have a Social Security number or an individual tax ID number. These numbers help the IRS identify individuals for tax purposes. As an employer, the Social Security Administration (SSA) allows you to verify Social Security numbers online, over the phone, or by submitting a paper request. If you have questions or need help utilizing one of the verification methods, call the SSA.[5]

-

4File each employee's W-4. A W-4 is an IRS form employees fill out and submit to you so you know how much federal income tax you need to withhold from each employee's paycheck. W-4 forms can be found on the IRS website.[6] The amount you withhold will depend on his or her filing status and the withholding allowances claimed.

- Ask each employee to fill out a W-4 upon hiring them. Keep all of them on file as you may be required to submit copies to the IRS upon request.

- If an employee does not submit a W-4, withhold tax as if they are single with zero withholding allowances.[7]

Withholding Employment Taxes

-

1Determine what wages are taxable. When it comes time to pay your employees, you will need to withhold a certain dollar amount from each employee's paycheck. To determine how much to withhold, you first need to know what wages are taxable. While each state will have different rules concerning what taxable wages are, most states will follow the federal rules. In general, any pay given to an employee for services performed are subject to federal and state income tax. The pay does not need to be in cash and might be in the form of goods, lodging, food, or clothing. An employee is anyone you pay for services and you control how, when, or where the work is done.

- For example, assume you employ two people. One person is considered an independent contractor under federal law (i.e., not an employee) and gets paid with food and lodging. The second person you employ gets paid in money every other week for services they provide at your direction (i.e., they are an employee). In this scenario, only the second person's wages are subject to federal and state income tax withholding.

-

2Calculate each employee's total wages. On payday, you will need to use each employee's total wages for the pay period in order to accurately withhold taxes. For state income tax purposes, if you employ nonresidents of the state you conduct business and pay taxes in, you should only include the nonresident's wages paid for work performed in your state.[8] For federal income tax purposes, you can include everything.

- For example, if your only employee gets paid every other week, their pay period will be a two week window. Assuming they are a resident of the state you conduct business and pay taxes in, you should include all forms of wages in the calculation. Assume your employee gets paid $1,200 per pay period in money as well as $800 per pay period in lodging expenses. This employee's total wages would equal $2,000 per pay period.

-

3Validate each employee's federal and state withholding allowances. Look back at every employee's W-4 to determine their withholding allowances and marital status. You will need this information, in addition to total wages, in order to determine how much to withhold.[9] While the W-4 is a federal document, most states will accept it. However, some states have their own withholding form that should be used if it is available. If a state form is available, the federal form cannot be used to calculate state withholdings.[10]

- For example, assume you are in a state that accepts the federal W-4, and that is the only withholding form you have on file for your employee. Assume your employee has a marital status of "single" and takes a total number of allowances equaling four.

-

4Determine how much state income tax to withhold. Using every employee's total wages, marital status, and total allowances, you will determine the state income tax to be withheld on each paycheck. This determination will be made using a state income tax withholding table. The tables can be found on your state's department of revenue website.

- For example, in Minnesota, there are multiple tables and you will use the one that corresponds to your employee's marital status pay period. If the employee is single and gets paid twice a month, you will use the Minnesota table that corresponds to that information. When you find that table, you will locate the intersection between the total number of allowances your employee takes and the total wages they make. The number you land on will be the amount you withhold. If your employee takes four withholding allowances and makes $2,000 every two weeks, you will withhold $75 for state income tax.[11]

-

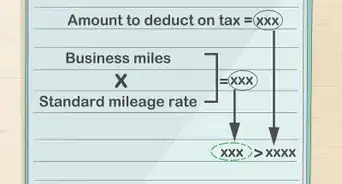

5Calculate federal income tax withholding. There are multiple ways to calculate the federal withholding amount, but one of the most common ways is using the "percentage method." To use this method, you will multiply one withholding allowance for your payroll period (using a specific table in IRS Publication 15) by the number of allowances each employee claimed on their federal W-4. You will then subtract that amount from each employee's wages. Finally, using another table, you will determine how much to withhold.

- For example, assume your only employee claims four allowances on their W-4, they are single, and they are paid $2,000 in total wages every other week. One allowance, according to the IRS table, is $168.80. When you multiply this number by four, you get $675.20. Next, when you subtract $675.20 from $2,000, you get $1,324.80, which is the amount subject to federal income tax withholding. Using IRS Publication 15, you will then find the table that corresponds to a single person who gets paid biweekly. Next, find the wage range that corresponds to your employee's wage, after subtracting your allowances, and calculate the tax based on your findings. In this instance, you would withhold $167.87 from your employee's paycheck.[12]

-

6Include supplemental payments you made to each employee. Some states will also require you to withhold a certain percentage of payments you make to the employee in addition to normal wages. Examples of supplemental payments include overtime, commissions, and bonuses. In Minnesota, for example, you are required to withhold 6.25% of every employee's supplemental pay.[13]

- For example, assume you paid your only employee a $2,000 bonus (on top of their total wages) in a single pay period. In this instance, you would withhold an extra $125 ($2,000 x .0625) in addition to the state and federal income tax you have already withheld.

-

7Withhold federal social security and Medicare taxes. In addition to withholding federal and state income tax, you also need to withhold federal social security and Medicare taxes from your employees' wages. For 2016, you are required to withhold 6.2% for social security taxes and 1.45% for Medicare taxes.[14]

- For example, if your employee's total wages are $2,000, you would be required to withhold $124 for social security taxes ($2,000 x .062) and $29 ($2,000 x .0145) for Medicare taxes.

-

8Use a tax calculator when available. Some states offer an online tax calculator to help you calculate your state tax withholding responsibilities. If your state offers this resource, use it. For example, in Minnesota, you can visit the Department of Revenue website and use their tax calculator to help.[15]

Depositing Employment Taxes

-

1Consider hiring a payroll specialist. Payroll service providers can be hired to control your funds in order to deposit withheld taxes and file returns on your behalf.[16] These services can be incredibly helpful if you do not have a finance background or if you don’t want to take time away from other business tasks. The cost of these services will vary from location to location, but the fee structure is usually the same. You will usually have to pay a flat monthly fee in addition to charges for each employee you have.

- Flat fees can range from $20 to $100 depending on the services they are performing for you. The per employee charge usually ranges from $1 to $10.[17]

-

2Determine which deposit schedule you are required to use. At least once per month you will be required to deposit your withheld funds with the IRS and state department of revenue. To determine how often you have to deposit your withheld funds, you will need to follow the rules laid out in IRS Publication 15. In general, if you reported $50,000 or less of taxes during your lookback period (usually the prior year), you will deposit once per month. If you reported more than $50,000, you will report semiweekly.

- The amount you report is the total federal income, Medicare, and social security tax you withheld from every employee you have combined.[18]

- Your state deposit schedule will usually coincide with your federal schedule. Therefore, if you deposit monthly with the IRS, you will also deposit monthly with your state department of revenue.[19]

-

3Gather the withheld funds in a secure business account. All funds you withhold from your employees’ paychecks should be stored in a business account designated for withheld funds. You should never commingle withheld funds with your personal accounts. When it comes time to deposit money, the funds will be taken out of this account.

-

4Deposit your state withholdings with the state. Most states will require you to make your deposits electronically if you meet certain criteria. For example, in Minnesota, you are required to deposit electronically if you withheld $10,000 or more in the previous year, you are required to pay electronically by another state department, or if you use a payroll service company.

- Be sure you deposit your funds in a timely manner or you may be subjected to late fees. In Minnesota, if you are late depositing your funds, you will be required to pay a 5% penalty on the entire sum of your deposit due.[20]

-

5Deposit your federal withholdings with the IRS. The IRS requires everyone to transfer their funds electronically in order to make deposits. When the due date comes, make sure you make your transfer on time or you will be assessed a federal penalty. If you are one to five days late, you will owe an extra 2%. However, the penalties can be as high as 15% in some circumstances.[21]

Filing Returns

-

1Determine your reporting due dates. In addition to depositing funds with your state and federal government, you must also file quarterly or annual employer tax returns with your state and the federal government. Every state and the federal government will have different rules regarding when you have to file.

- The IRS requires you to file quarterly returns unless they notify you otherwise or unless a federal exception applies. The exceptions apply to agricultural employers, seasonal employers, household employers, or employers reporting wages for employees living in territories of the United States.[22]

- A state like Minnesota also requires quarterly employer tax returns unless your filings are for minimal amounts ($500 or less).[23]

-

2Gather the required state and federal documents. In general, so long as you are required to file quarterly returns, you will fill out IRS Form 941.[24] Each state will have their own forms you need to get ahold of as well. Minnesota has a worksheet you need to fill out, which can be found online.[25]

- If you file annually, you will need IRS Form 944 instead of Form 941.[26]

-

3Fill out the forms. The purpose of these forms is to ensure you are paying the employer taxes required and to get any refund if you have overpaid. Federal and state employer tax returns ask you information about your business as well as your quarterly deposits.[27] When you fill out your forms, make sure you fill them out accurately and completely. Any mistakes could cause your return to be delayed and you might even have to pay a penalty. Generally, you will need the following information in order to fill out your returns:[28]

- Your employer identification number

- The number of employees you have

- The wages you paid

- The taxes withheld

- Your usual deposit schedule

-

4File the forms. The federal return can be filed online or by mail. If you are filing online, you will use the IRS e-file service.[29] If you are mailing your return in, you will mail it to a designated address that will vary depending on where your business is located and whether you are making a payment. You can look at the instructions for IRS Form 941 for more information.[30]

- Some state returns must be filed electronically or over the phone. Other states will allow paper submissions. For example, in Minnesota, employer returns must be filed electronically or over the phone.[31]

-

5Prepare your W-2s at the end of the year. At the end of each year, you will be required to prepare and file IRS Form W-2 to report income you paid to employees. This information will be reported to the IRS and the SSA.[32] Each of your employees must receive a copy of their personal W-2 by January 31st of each year.[33]

- Form W-2 can be found on the IRS website.[34]

-Step-9.webp)

References

- ↑ https://www.irs.gov/pub/irs-pdf/fss4.pdf

- ↑ https://www.revenue.state.mn.us/sites/default/files/2020-01/factsheet10.pdf

- ↑ https://www.uscis.gov/sites/default/files/files/form/i-9.pdf

- ↑ https://www.revenue.state.mn.us/sites/default/files/2020-01/factsheet10.pdf

- ↑ https://www.revenue.state.mn.us/sites/default/files/2020-01/factsheet10.pdf

- ↑ https://www.irs.gov/pub/irs-pdf/fw4.pdf

- ↑ https://www.revenue.state.mn.us/sites/default/files/2020-01/factsheet10.pdf

- ↑ https://www.revenue.state.mn.us/sites/default/files/2015-12/wh_inst_16.pdf

- ↑ https://www.revenue.state.mn.us/sites/default/files/2015-12/wh_inst_16.pdf

- ↑ https://tax.thomsonreuters.com/blog/accounting-audit-payroll/payroll/federal-and-state-w-4-rules/

- ↑ https://www.revenue.state.mn.us/sites/default/files/2015-12/wh_inst_16.pdf

- ↑ https://www.irs.gov/publications/p15/ar02.html#en_US_2016_publink1000254685

- ↑ https://www.revenue.state.mn.us/sites/default/files/2015-12/wh_inst_16.pdf

- ↑ https://www.irs.gov/publications/p15/ar02.html#en_US_2016_publink1000202402

- ↑ http://www.revenue.state.mn.us/Forms_and_Instructions/wh_inst_16.pdf

- ↑ https://www.revenue.state.mn.us/sites/default/files/2015-12/wh_inst_16.pdf

- ↑ http://www.businessnewsdaily.com/7477-choosing-payroll-service.html

- ↑ https://www.irs.gov/publications/p15/ar02.html#en_US_2016_publink1000202435

- ↑ https://www.revenue.state.mn.us/sites/default/files/2015-12/wh_inst_16.pdf

- ↑ https://www.revenue.state.mn.us/sites/default/files/2015-12/wh_inst_16.pdf

- ↑ https://www.irs.gov/publications/p15/ar02.html#en_US_2016_publink1000202468

- ↑ https://www.irs.gov/publications/p15/ar02.html#en_US_2016_publink1000202497

- ↑ https://www.revenue.state.mn.us/sites/default/files/2015-12/wh_inst_16.pdf

- ↑ https://www.irs.gov/pub/irs-pdf/f941.pdf

- ↑ https://www.revenue.state.mn.us/sites/default/files/2015-12/wh_inst_16.pdf

- ↑ https://www.irs.gov/publications/p15/ar02.html#en_US_2016_publink1000202497

- ↑ https://www.irs.gov/instructions/i941/ch01.html

- ↑ https://www.irs.gov/pub/irs-pdf/f941.pdf

- ↑ https://www.irs.gov/publications/p15/ar02.html#en_US_2016_publink1000202497

- ↑ https://www.irs.gov/instructions/i941/ch01.html#d0e571

- ↑ https://www.revenue.state.mn.us/sites/default/files/2015-12/wh_inst_16.pdf

- ↑ https://www.irs.gov/businesses/small-businesses-self-employed/understanding-employment-taxes

- ↑ https://www.revenue.state.mn.us/sites/default/files/2015-12/wh_inst_16.pdf

- ↑ https://www.irs.gov/pub/irs-pdf/fw2.pdf

About This Article