This article was co-authored by Carla Toebe. Carla Toebe is a licensed Real Estate Broker in Richland, Washington. She has been an active real estate broker since 2005, and founded the real estate agency CT Realty LLC in 2013. She graduated from Washington State University with a BA in Business Administration and Management Information Systems.

There are 18 references cited in this article, which can be found at the bottom of the page.

This article has been viewed 88,080 times.

Investing in real estate has become a popular way of building an investment portfolio. Historically, real estate investments perform better than some other kinds of assets. It also presents the prospective investor with several different options. To get into real estate, you can become a landlord and purchase property yourself, but can also make money by buying into a Real Estate Investment Trust (REIT) or lending to other real estate investors.

Steps

Becoming a Landlord

-

1Take stock before you invest. Investors should know how they intend to dispose of any property before they buy it. Do you want to flip the property and resell it? Or, do you want to rent the property? These options have different implications when it comes to financing and taxes; you’ll need to have a general idea of what direction you want to take at the outset and be ready for contingencies.

- You’ll need a realistic sense of your skills set, for one thing. Do you have the technical skills and knowledge to flip properties? You’ll need to have a basic knowledge of property repairs and of the costs of typical and less typical repair work.

- Having a reserve fund is also a MUST, whether you intend to rent or to flip the property. As a rule, an investor should have enough money in reserve to pay the mortgage for six months in case the property ends up vacant or is in a rehab-to-sell situation. When you rent, you also depend on timely payment to cover the mortgage. A reserve will help you cover the payment if your tenant’s rent happens to be late.

-

2Analyze profitability of available properties. Before diving into the purchase of a property, make sure it is going to be a profitable investment. Evaluate your operating expenses and the amount of rent or income you expect to receive. Consider the neighborhood where you want to buy to determine if properties retain their value in that location.[1]

- Calculate the price-to-rent ratio in the neighborhood where you want to purchase. Keep in mind that information on rent prices is not always easy to obtain, so this number should only be considered a ballpark figure. Divide the median home price by the median annual rent. For example, suppose the median home price is $180,000, and the median annual rent is about $12,000 ($1,000/month). The price to rent ratio is . The lower the ratio, the better the investment is. An area with a price to rent ratio over 20 is not a good investment.[2]

- Calculate gross rental yield. Divide the annual rent by the total purchase price of the property. This helps you find the house with the highest rental income and the lowest purchase outlay. For example, if you pay $100,000 for a house and you can collect $12,000 in rent per year ($1,000/month), the gross rental yield is 12 . Anything above 10% is a good investment.[3] Some properties may require a significant amount of capital investment to make it livable (a new roof, replacing carpeting, etc.), but a high enough rental yield can still make a property that requires work a good investment.

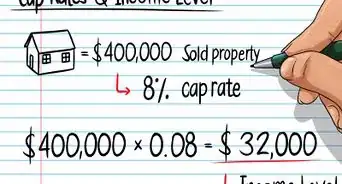

- Calculate the capitalization rate. This tells you the rate of return on the property’s income. The capitalization rate is typically based on the property’s net income in the most recent year (if it is being rented) or on the projected rental income (if it is not currently being rented). Divide the net operating income by the purchase price of the property. The net operating income is the total annual revenue minus operating costs (operating costs tend to use up about 40% of the income). Suppose you want to purchase a property for $500,000 and your net operating income would be $35,000. Your capitalization rate would be 7% . This means that you would earn 7% of the value of the property as profit. Use the capitalization rate to compare the profitability of different properties.[4]

- If the operating costs are not clear, or you're just trying to get a very general idea of whether or not the property is a good investment, take the purchase price divided by the total yearly rent to see how many years it will take to earn the money back. This can help you compare properties — if one property will take five years to earn back the investment and another property will take seven years, and capital improvements are equal, then you will likely want to pursue the property that will earn your money back faster.

- Calculate cash flow. Figure out if you will make enough income in rent to cover the mortgage principal, interest, taxes and insurance. Also, make sure you have enough in reserve to cover unexpected expenses like repairs. If not, your cash flow will be negative, which means you would be in danger of defaulting on your mortgage.[5]

Advertisement -

3Arrange Financing. First, you will likely need to put down a large percentage as a down payment – many commercial loans require between 25% to 35% down payments. If you don’t have that much cash on hand, look into getting the money from a home equity line of credit, personal loan, credit cards or by cashing in a life insurance policy. Lenders will determine your interest rate based on your credit score and the amount of financial reserves you have in the bank to cover expenses on the property. Consider working with a neighborhood bank instead of a large, national bank. Local banks often offer more flexibility in structuring a mortgage.[6]

- A 20% down payment is not your only option. You may be able to get FHA owner-occupied financing with as little as a 3.5% down payment. There are also hard money loans – these can often get you financing very fast, as the loans aren’t based on your credit score, but they carry a higher interest rate typically near the usury rate. Hard money loans may work for house flips but aren’t recommended for long-term investments.[7] [8]

- Your best bet is to sit down with a professional broker to learn about your different financing options. There are numerous restrictions as well as limits on conventional loans for investors. You generally can only have one FHA loan at a time, for instance, and are legally required to take out commercial loans for buildings with 5 or more units. A broker can help you navigate your options and help you strategize to make sure all your funding needs are covered.

- Be upfront with lenders about the state of the property. Many banks will not fund on particular types of property, so to avoid having your funding fall through down the line, provide the lender with photos and information on any issues with the property. You don't want the deal falling apart when the lender does an appraisal and finds out there is extensive damage on the property or that it needs repairs.

- Note that mortgage insurance – which protects the lender in case of default – will not cover investment properties.

-

4Shop for a property. Start by looking at the properties listed on the multiple listing service (MLS). You can find the MLS listings on websites like Realtor.com, Trulia, or Zillow. You will find all of the same listings on your own on the MLS that a real estate agent could find for you. However, it’s still a good idea to work with a Realtor. They may have more information about amenities or specific properties. Also, they will know about available properties that are not listed on the MLS.[9]

- One of the biggest advantages of working with a Realtor is that they will give you an edge when it comes to timing. They can set you up to get immediate emails for listings that meet your criteria as soon as they go on the market or back on the market, and before they appear on other websites. This is valuable service in a tight real estate market.

- Be aware that there are certain things a Realtor cannot legally comment on. Your Realtor could not, for instance, make a judgement about whether a neighborhood is "good" or "bad." Use a resource like RAIDS online to check crime in the area or floodsmart.gov to find out if flooding is common (requiring you to buy additional flood insurance for your property).

- Realtors are often paid by the seller at settlement, so it’s sometimes free for the buyer to work with one. But buyers may also pay a real estate commission to a buyer’s agent. This can be a negotiated item in a “For Sale by Owner” transaction and may open up other available properties for you to consider.

-

5Make your offer. Work with your real estate agent to determine a fair price for the property. Also, write in contingencies for inspection, financing, and any other contingencies that your Realtor or lawyer advise. Choose a settlement date that works well for you and for the seller. Some sellers will accept an offer with a lower price if the offered settlement date is convenient.[10]

- Always have a property inspected to find any problems that may cost you money in the future. If the inspector finds anything, you may be in a position to renegotiate. You may be able to lower your offer and make the needed repairs yourself, request the seller make the repairs, or a combination of both.[11]

- Disclose everything about the inspection. Some lenders won’t finance a property if they are aware of a needed repair that is important to them, for instance. It’s best to resolve everything before closing or move on to other properties if problems arise and aren’t fixed to your satisfaction.

- You’ll usually want to be sure that the property passes inspection and all other requested contingencies. However, there are some circumstances when a buyer might waive contingencies and purchase a property anyway. For example, some investors are willing to do repairs and don’t need financing; they may buy a property that wouldn’t pass inspection.

-

6Find tenants. If you’re intending to rent the property you’ll need to find tenants, ideally ones who will pay their rent in full and on time, keep your property in good condition, and will follow the policies outlined in your lease. Consider several factors in your search for tenants. Advertise for tenants without discriminating against any groups. Screen tenants thoroughly.[12]

- Advertise your property by word of mouth, flyers, signs, print ads in local newspapers and online ads on real estate websites. Websites like Craigslist, Zillow, and others allow free posting of rentals.

- Charge enough rent to cover your operating expenses, earn a reasonable profit and to be competitive with other rentals in the area. You must use the same criteria for everyone.

- Provide applicants with a list of the rental criteria that they will be evaluated against.

- Have any applicants fill out an application that lists not only their contact information, but also their sources of income, previous addresses and names of references. Also, get their permission to verify their income and check their credit. Once you have permission, check with their employers to verify their income. Once you have their Social Security number and permission, you can check their credit with any of the three credit reporting bureaus. Contact previous landlords to check references.

-

7Screen applicants. You are able to screen rental applicants according to disqualifying criteria. These can include credit score, gross income, criminal history, and rental history. A previous eviction could mean denial, for example, or owing money to an earlier landlord. Be sure to give applicants a complete list of the criteria you’re using to evaluate them – these criteria are up to you, so long as you don’t discriminate against any protected groups or violate state or federal law.

- Understand any federal, state and local laws that protect certain classes of people from discrimination. For example, the Civil Rights Act prevents discrimination on the basis of race. The Fair Housing Act ensures fair treatment no matter someone’s race, color, national origin, religion, sex, disability or if they have children.

- If you decide to approve an applicant with issues, you can insist on certain conditions like a larger deposit or a co-signer. However, if you deny or approve an applicant with extra conditions, they’ll need an adverse action letter explaining the reasons why.

- There are companies that can provide professional screening. Applicants usually pay for this service themselves, leaving you out of the investigative process. Then, once you get the results, you can evaluate further and decide on any extra conditions.

-

1Understand the meaning of real estate investment trust (REIT). REITs are companies that own or manage commercial real estate. They allow individuals to profit from real estate income without having to purchase commercial real estate.[13]

-

2Choose a type of REIT in which to invest. REITs are available in a number of different industries. REITs in each industry have their own way of earning income from the real estate. When choosing a type of REIT, evaluate the strength of the overall economy and how that industry is performing.[14]

- Retail REITs include shopping malls and freestanding stores. They make money from the rent they charge to tenants. Choose to invest in retail REITs when the retail industry is strong and sales are high.

- Residential REITs own multi-family apartment buildings. They also make money from charging rent to tenants. Residential REITs are most profitable in large urban areas where home prices are so high that many people are forced to rent. This drives rent prices up and increases profitability for the REIT. Job growth in the area affects the profitability of a residential REIT, as well as things like vacancy rate, number of building permits issued, and if there is rent control.

- Healthcare REITs invest in hospitals, nursing homes, medical centers and retirement homes. These are becoming more profitable as people are starting to live longer and need more of these services. They make money from the healthcare system.

- Office REITs own office buildings. Their income comes from long-term leases in the office buildings. Consider the state of the economy and the unemployment rate before investing in an office REIT. Also, evaluate the economic status of the area where the REIT is. Some cities are economically depressed, while others are experiencing economic growth.

- Mortgage REITs invest in mortgages and mortgage backed securities instead of in property.

-

3Purchase shares in an REIT. Contact a broker or financial planner to find the right REIT investment for you. REIT investments can be purchased through a variety of different avenues. Some are publicly traded on a stock exchange. Others are not listed or are privately traded. Another option is to purchase shares in an REIT mutual fund or exchange traded fund (ETF).[15]

- Many REITs are registered with the Securities and Exchange Commission (SEC) and listed on major stock exchanges such as the New York Stock Exchange (NYSE).[16]

- Public non-listed and private REITs are registered with the SEC, but they are not listed on a stock exchange.[17] [18]

- If you don’t want to worry about choosing a specific REIT in which to invest, choose to purchase shares in an REIT mutual fund or exchange traded fund. These are available from investment companies such as Vanguard, Fidelity or JPMorgan Chase & Co. The investment company researches the real estate market and builds a portfolio that will earn the highest return.[19]

Lending Money to Other Real Estate Investors

-

1Understand the meaning of private money lending. Private money lending means lending your own money to another investor or to a professionally-managed real estate fund. This might appeal to you if you have already made some money with your other real estate investments, and you are looking for a way to re-invest some of those funds. As a private money lender, you act as an alternative to a bank or other financial institution. The loans you make are secured by real estate.[20]

- Investors like to work with private money lenders because they can get money quickly without the strict regulations imposed by banks. Also, the process is generally very transparent.

- Private money lenders – often called hard-money lenders – charge higher rates than banks and expect to be repaid in less time, usually around 5 years. They’re meant for investors who tend to flip properties rather than rent, unless you sell before the mortgage is due. However, they often take on higher-risk loans that a bank wouldn’t authorize, such as loans for properties the person plans to rehab and then sell or rent.

-

2Identify borrowers. Private money lending is becoming a significant source of financing in the real estate industry. As banks and other lending institutions impose more strict regulations, investors are turning more frequently to private money lenders to get money quickly. Borrowers come from different sectors in the real estate industry.[21]

- People looking to flip houses, for instance, often seek these types of loans because the current condition of the property is not relevant. In these cases, will need to know the current value of the property and the expected value after it is rehabbed. Make sure you get a valuation from a licensed Realtor or an appraiser.

- Builders, developers and commercial investors turn to private money lenders to fund their development projects. Banks tend to shy away from these kinds of speculative investments.

-

3Mitigate risk. Evaluate potential loans to see whether they are going to be profitable investments. Consider several factors when deciding whether or not to pursue an opportunity. Failure to carefully weigh the risks against the potential profits can result in loss of capital.[22]

- Most private money loans are between 60 and 70% of the market value of the property. The ratio of the loan to the market value of the property is known as the loan-to-value ratio.

- In addition to evaluating the creditworthiness of the borrower, research their equity. Find out if they have enough equity in other properties to cover emergencies or unforeseen expenses.

- Wherever possible, structure the loan so that you are in the first lien position. This means that you are the first creditor to receive remuneration in the event of a default. You can secure this lien priority if you offer a higher loan-to-value ratio.

-

4Generate the proper loan documents. The paperwork involved in a private money loan is similar to that of a typical loan from a bank. The borrower must sign a promissory note, which is a promise to repay the loan. In addition, the borrower must put up collateral for the loan in the form of a mortgage. Private money loans for residential real estate often require third-party appraisals, an in-person property inspection, and a geology report, among other things. Check with your lender to determine their requirements. You might also need the following documents:[23]

- A letter of intent (LOI) outlines the agreement.

- A purchase and sale agreement state the final price and the terms of the purchase.

- A preliminary title report lists the history of the property’s ownership; title insurance is also required.

- Proof of funds is a bank statement or other document produced by the borrower to ensure they have the funds available to repay the loan.

- A personal guarantee from the borrower states which assets the borrower can liquidate if the loan can’t be repaid.

- A deed of trust or mortgage pledges property to secure the loan.

- An environmental indemnity agreement is an agreement by which the borrower agrees to compensate you for any losses from environmental contamination of the property.

References

- ↑ http://www.investopedia.com/financial-edge/0511/8-must-have-numbers-for-evaluating-a-real-estate-investment.aspx

- ↑ http://www.investopedia.com/financial-edge/0511/8-must-have-numbers-for-evaluating-a-real-estate-investment.aspx

- ↑ http://www.bankrate.com/finance/real-estate/gross-yield-rental-house.aspx

- ↑ http://www.investopedia.com/terms/c/capitalizationrate.asp

- ↑ http://www.investopedia.com/financial-edge/0511/8-must-have-numbers-for-evaluating-a-real-estate-investment.aspx

- ↑ http://www.bankrate.com/finance/real-estate/5-tips-for-financing-investment-property-1.aspx

- ↑ https://www.biggerpockets.com/renewsblog/2015/10/01/real-estate-strategy-newbies/

- ↑ https://www.biggerpockets.com/renewsblog/2006/12/08/what-does-everyone-mean-by-hard-money/

- ↑ https://www.biggerpockets.com/renewsblog/2013/02/22/buying-rental-property/

- ↑ https://www.biggerpockets.com/renewsblog/2010/03/24/7-tips-for-better-real-estate-negotiation/

- ↑ https://www.biggerpockets.com/renewsblog/2013/02/22/buying-rental-property/

- ↑ http://www.investopedia.com/university/the-complete-guide-to-becoming-a-landlord/finding-tenants.asp

- ↑ https://www.investor.gov/investing-basics/investment-products/real-estate-investment-trusts-reits

- ↑ http://www.investopedia.com/articles/mortgages-real-estate/10/real-estate-investment-trust-reit.asp

- ↑ https://www.reit.com/investing/investing-reits/how-invest-reits

- ↑ https://www.reit.com/investing/investor-research/reit-directories/searchable-directory

- ↑ https://www.reit.com/investing/reit-basics/public-non-listed-real-estate-companies

- ↑ https://www.reit.com/investing/reit-basics/private-real-estate-companies

- ↑ http://money.usnews.com/money/blogs/the-smarter-mutual-fund-investor/2015/10/09/how-to-invest-in-commercial-real-estate-with-reits?page=2

- ↑ http://www.fortunebuilders.com/becoming-private-money-lender-part-1/

- ↑ http://www.fortunebuilders.com/becoming-private-money-lender-part-1/

- ↑ http://www.fortunebuilders.com/becoming-private-money-lender-part-2-breaking-private-money-loan/

- ↑ http://www.fortunebuilders.com/becoming-private-money-lender-part-2-breaking-private-money-loan/

About This Article