wikiHow is a “wiki,” similar to Wikipedia, which means that many of our articles are co-written by multiple authors. To create this article, 14 people, some anonymous, worked to edit and improve it over time.

This article has been viewed 146,160 times.

Learn more...

Going through the process of buying or selling a house without the assistance of a real estate agent can be tricky. However, it can also save a large amount of money. By carefully moving through the process and taking time to learn, you can successfully close your own real estate deal. Note that the a mortgage company or the buyer might require a closing agent and not allow you to do this on your own.

Steps

Gathering Documents

-

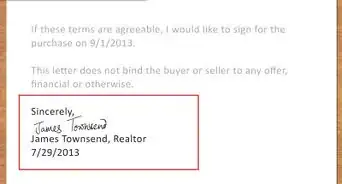

1Draft a purchase and sale agreement. A purchase and sales agreement is a fairly long document outlining the basic terms of the deal you're making with a buyer or seller. While most professional real estate agents use a very lengthy document, if you want to do a closing yourself you can pack the necessary information into one to two pages by sticking to the basics. Search for "real estate purchase and sale agreement template" online to find examples and usable templates. All you need to include are:

- The date of the agreement, the agreement's expiration date, and when the transaction will close. This should include rights of inspection and who pays for such, if any, costs.

- The price of the property and the means (cash, check, etc.) that amount will be paid.

- The state, county, parcel number, and legal description of the property being bought or sold.

- The name and signature of the buyer and seller.

- Details on which party will pay closing costs like property taxes, title work, recording fees, etc.[1] Include escrow amounts and conditions to close, including right of buyer or seller to renege on transaction (such as if the house is found to have major structural damage).

-

2Obtain a title search. If you're buying or selling a property, you need to obtain or issue an insurance policy title. Unless you're really familiar with real estate dealings and have professional experience in the field, it's best to hire a title insurance firm to do research and issue a policy.[2]Advertisement

-

3Get a deed. A deed is the most fundamental document of a real estate transaction. It is the document that determines who owns the property and the expectations of the buyer and seller. If you plan and drafting a deed yourself, it's vital to include the following:

- A statement that entitles the owner to the property, basically a short opening statement saying the time and date the buyer gained ownership of the lot or house.

- A list of property rights from one person to another, that is what rights the buyer does and does not have regarding how he or she uses the property

- A definition of what ownership of a property means in that specific region's governing body, that is a brief overview of property laws in your state, city, etc.[3]

- Once a deed is signed and completed, you need to take it to the local courthouse where it can be signed and notarized. Which precise office of the court or county notarizes deeds varies from state to state and county to county, but someone at the courthouse should be able to provide the information. You can also find this information online through your local state government's website.[4]

-

4Check if any supporting documentation is needed. Laws regarding property tend to vary by state. Some states require supporting documentation. Usually, these documents inform city officials like a county treasurer of the price of the property or finalize the fact the property's been transferred to a new owner. Ask at the courthouse about any supporting documents you may need. You can also find this information at your state's website.[5]

-

5Make sure you've used the proper template. Documents regarding real estate transactions come in a specific template. Depending on the state, the forms may need to be designed in a very specific format. USLegal, a software program that helps you format legal documents, can be used to assure the template is correct. You can also download some templates online or talk to an attorney or real estate agent about proper formatting.[6]

Starting the Closing Process

-

1Open escrow. An escrow account is an account held by a third party on behalf of the two parties involved in a transaction. An escrow account is the best way to assure both the buyer and the seller get a fair deal regarding the transaction.[7]

- Money should not be exchanged between buyer and seller in a real estate transaction until the sale is finalized. An escrow account is where any money goes in the meantime, and an escrow agency manages the account.

- You can find escrow agencies online and in the yellow pages. Make sure to read reviews. You may even want to ask a representative for the phone numbers of previous clients so you can ask people one-on-one about their experience working with the agency.

-

2Decide if you want an attorney. If you're not well versed in the real estate game, you may want to hire professional legal consultation to review any and all documents for you. If you want help, seek out a real estate attorney in your area. As with an escrow company, read reviews online and seek out the opinions of past clients.[8]

-

3Negotiate closing costs. As you near the end of negotiations regarding the selling price of a home, you'll have accrued some closing costs from the escrow company. While you cannot expect the company to perform duties for free, many escrow companies take advantage of ignorant buyers and sellers to slap on junk fees. Know how to negotiate with the escrow company regarding closing costs.

- Look out for fees with names like application review fees, appraisal review fees, processing fees, and settlement fees. Start off negotiation by asking an escrow agent what precisely these fees are for. If the agent is worried you're suspicious, he may offer to waive or reduce the fees. Escrow agencies want to maintain a solid reputation and do not want buyers and sellers complaining to others in the real estate world of junk fees.[9]

-

4Inspect the home. Once you're moving towards closing, you'll need to conduct a home inspection. You want to make sure no repairs or renovations are needed before closing the deal.

- Unless you have knowledge of home inspection and repair, you'll have to hire a third party to conduct the inspection. Issues like faulty wiring and poor plumbing, which could pose major problems down the road, might go overlooked by the untrained eye.[10]

- A home inspection agency will, for a small fee, look over a home and report back any outstanding issues. If there is anything major, like big structural problems that require costly repairs, you can ask the seller to pay for these before you close the deal.[11]

-

5Check for pests. You should also have a professional exterminator inspect the home for signs of pests before closing a deal. Problems like termites and bed bugs can be incredibly difficult to get rid of and rats and mice are unsanitary. Any major pest problems should be eliminated by the seller before you close on a home.[12]

Finishing Up

-

1Renegotiate, if necessary. Depending on the results of your inspection and your closing conditions (unless spelled out in the paper work, property may be "as is"), you may need to renegotiate your offer. Certain issues, like bug and structural damage, may mean you'll want to pay more or less for the home.

- If anything came up in inspection, you have two options. You can pay less for the home, given that you'll have to pay for costs of repairs. You can also ask that the seller have repairs made before you finalize the deal and pay the originally agreed upon price.[13]

- Repair companies and pest removal companies can often only give an estimated cost. This can make renegotiating the price given cost of repairs difficult. The best option is to ask that the seller have repairs made before finalizing the deal. This assures you will not spend more money than necessary.[14]

-

2Figure out the interest rate. You need to lock down an interest rate before finalizing a real estate deal. Interest rates are unpredictable and tend to fluctuate over time, so try to lock down a low rate before signing any official paperwork.[15]

-

3Fund escrow. When you initially started negotiating your deal, you likely had to put down earnest money if it was included in the purchase and sale agreement. This is money put down in your escrow account to convey an earnest interest in purchasing the property. The earnest money usually goes towards funding escrow as well as your down payment. As you move towards the closing process, you need to pay any remaining escrow fees.[16]

-

4Do a final walk through. Before signing all your papers, do a final walkthrough of the property. Make sure no damage was done, any repairs you asked for were made, and nothing was removed or changed against your will.[17]

-

5Sign the papers. Once you've completed all else involved, there is nothing left to do but sign the papers. While this may seem like a simple process, there are a few things you should be aware of going in.

- Real estate closings can be complicated. There may be over 100 pages of paperwork. While you do not have to read everything, make sure things like interest rates, down payments, closing costs, and your rights are what you agreed upon during the closing process.[18]

- If there is anything you don't understand about the real estate paperwork, consult a real estate attorney.[19]

Community Q&A

-

QuestionWhat is a simple way to close a small farm my brother wants to buy from my mother in cash without using an attorney? All siblings have power of attorney and agree with the purchase.

Community AnswerGet a realtor and ask him/her to charge 1% because the sellers and buyer are on the same page. Otherwise, you may want to get the right documentation and ask a title company to help you with the documentation.

Community AnswerGet a realtor and ask him/her to charge 1% because the sellers and buyer are on the same page. Otherwise, you may want to get the right documentation and ask a title company to help you with the documentation. -

QuestionHow do I look at a house without an agent and without using the listing agent as my agent?

Community AnswerIf the owner of the property has an agent, then you'll need a realtor to show it to you, but they do not have to be your agent. Remember, the seller has already agreed to pay 6% regardless of whether you have an agent or not. That agent doesn't always look out for your interests.

Community AnswerIf the owner of the property has an agent, then you'll need a realtor to show it to you, but they do not have to be your agent. Remember, the seller has already agreed to pay 6% regardless of whether you have an agent or not. That agent doesn't always look out for your interests.

Warnings

- Real estate closings are a complex process that requires a large amount of preparation and skill. If, at any time, you feel unsure of what you are doing or feel like you are over your head, consult a real estate agent or attorney to help you. Both real estate professionals will charge you for their assistance, but often their fees will be small compared to the cost of making a costly mistake by trying to handle a real estate closing on your own.⧼thumbs_response⧽

References

- ↑ http://retipster.com/how-to-close-cash-transaction/

- ↑ http://retipster.com/how-to-close-cash-transaction/

- ↑ http://retipster.com/how-to-close-cash-transaction/

- ↑ http://retipster.com/how-to-close-cash-transaction/

- ↑ http://retipster.com/how-to-close-cash-transaction/

- ↑ http://retipster.com/how-to-close-cash-transaction/

- ↑ http://www.investopedia.com/articles/mortgages-real-estate/10/closing-home-process.asp

- ↑ http://www.investopedia.com/articles/mortgages-real-estate/10/closing-home-process.asp

- ↑ http://www.investopedia.com/articles/mortgages-real-estate/10/closing-home-process.asp

- ↑ http://www.investopedia.com/articles/mortgages-real-estate/10/closing-home-process.asp

- ↑ http://www.investopedia.com/articles/mortgages-real-estate/10/closing-home-process.asp

- ↑ http://www.investopedia.com/articles/mortgages-real-estate/10/closing-home-process.asp

- ↑ http://www.investopedia.com/articles/mortgages-real-estate/10/closing-home-process.asp

- ↑ http://www.investopedia.com/articles/mortgages-real-estate/10/closing-home-process.asp

- ↑ http://www.investopedia.com/articles/mortgages-real-estate/10/closing-home-process.asp

- ↑ http://www.investopedia.com/articles/mortgages-real-estate/10/closing-home-process.asp

- ↑ http://www.investopedia.com/articles/mortgages-real-estate/10/closing-home-process.asp

- ↑ http://www.investopedia.com/articles/mortgages-real-estate/10/closing-home-process.asp

- ↑ http://www.investopedia.com/articles/mortgages-real-estate/10/closing-home-process.asp

About This Article

Doing your own real estate closing can take some work, but it will save you a lot of money. You’ll need to fill in your own purchase and sales agreement, but you can find templates online to save you time. Then, you’ll need to draft a deed, and get it signed and notarized. You should also hire a title insurance firm to issue an insurance policy title, since you won’t be able to do this yourself unless you have real estate experience. Check your state’s rules to see what supporting documentation you need, and make sure you have everything to close the sale. Don’t forget to have the property inspected for any expensive repairs that might affect its value. If there are any issues, you’ll want to renegotiate the cost. You’ll also need to open an escrow account to securely hold the money. For more tips, including how to make sure your documents are correct, read on!