This article was co-authored by Cassandra Lenfert, CPA, CFP®. Cassandra Lenfert is a Certified Public Accountant (CPA) and a Certified Financial Planner (CFP) in Colorado. She advises clients nationwide through her tax firm, Cassandra Lenfert, CPA, LLC. With over 15 years of tax, accounting, and personal finance experience, Cassandra specializes in working with individuals and small businesses on proactive tax planning to help them keep more money to reach their goals. She received her BA in Accounting from the University of Southern Indiana in 2006.

There are 7 references cited in this article, which can be found at the bottom of the page.

This article has been viewed 51,174 times.

Lots of people work for an hourly wage, but sometimes you might be asked how much you make a year. The question might stop you in your tracks at first, but it's actually pretty simple to get the answer.

Steps

Calculating Annual Salary

-

1Figure out if you are paid hourly. If you receive a pay rate per hour multiplied by the number of hours worked per week, then you are paid hourly. Another term for this is a non-exempt employee. The amount of your paycheck may change each week depending on how many hours you work. If your work hours do not vary but you are still paid by the hour, then you are still considered an hourly, or non-exempt employee even though your check is the same each week.[1]

-

2Determine how much you earn per hour. Your supervisor or someone in human resources can tell you how much you make per hour. If you don't want to ask, you can figure it out from your pay stub. Find where it tells you the total gross pay on your pay stub. This is how much you earned before taxes and benefits were taken out. Divide that amount by the number of hours you worked that week.

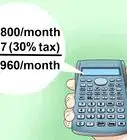

- For example, suppose your gross pay was $200 for a week in which you worked 10 hours. Calculate . Your hourly salary is $20 per hour.

Advertisement -

3Calculate your yearly pay if you work the same number of hours per week. Take your hourly salary and multiply it by the number of hours you work each week. This tells you your weekly salary. Multiply this by the number of weeks in a year, 52, to get your yearly salary.[2]

- If you work 40 hours per week and you earn $20 per hour, calculate your weekly salary with the equation .

- Then calculate your annual salary with the equation .

-

4Find the average if you work a different amount each week. If your hours vary every week, keep track of your weekly hours for about one month. Then calculate the average number of hours you worked each week. Multiply that by 52 to find your annual salary.

- If in one month you worked 30 hours the first week, 25 hours the second week, 35 hours the third week and 40 hours the fourth week, the average weekly hours is .

- If you earn $20 per hour, then your estimated annual salary is .

Adding in Other Kinds of Hours

-

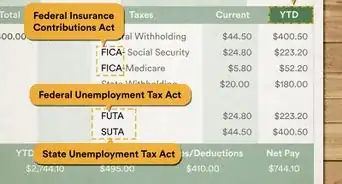

1Add in overtime hours if you earn them. If you work more than 40 hours per week and you are a non-exempt employee, you must be paid overtime. This means you earn one and a half times your regular pay for any hours over 40 hours per week. If you want to figure out how overtime affects your annual salary, keep track of your overtime and regular hours for at least a month. Figure out the average number of regular and overtime hours you work and multiply to get the total for the year. Add these two amounts together to get your total estimated annual salary.

- If in a 4 week period, you worked 50 hours, 45 hours, 42 hours and 47 hours, and anything over 40 hours is overtime, then your weekly overtime is 10 hours, 5 hours, 2 hours and 7 hours. Your average weekly overtime hours are .

- If you earn $20 per hour, then your overtime rate is

- Your average regular weekly salary is . Your average weekly overtime pay is . Your total weekly salary is .

- Your estimated annual salary is .

-

2Make modifications for sick time, vacation, or a leave of absence. If you get paid for vacation time or when you're out sick, then you don't need to make any changes to your annual salary. But if your employer doesn't pay you when you're out on vacation or sick, then this in effect changes the number of weeks you get paid in a year. If you take 2 weeks of vacation each year, then you work only 50 weeks per year instead of 52. You need to use 50 weeks to calculate your annual salary instead of 52.

-

3Calculate bonuses. Some companies pay bonuses at different times of the year. These are added to your regular salary. For example, your employer may give holiday bonuses, sign-on bonuses to new employees, or rewards for meeting goals. Also, sales commissions count as bonuses. If you earn bonuses, add them to your total when calculating your annual salary.[3]

- For example, suppose you earn an annual salary of $50,000 before bonuses, and your boss wants to give you a 2.5% holiday bonus. The amount of the bonus is .

- In this case, your total annual salary is .

Understanding Your Salary

-

1Figure out if you are earning enough. You have to know if your job is going to pay enough to support your lifestyle and think about your financial needs in order to make a budget. See if your annual salary is going to cover all of your bills. If not, see if there are ways to earn more money in the company. Find out if there is room for advancement in the company.[4]

- It's also important to understand if you are being paid enough in relation to your industry peers. Consult industry websites (like https://www.payscale.com/) that report average annual salary numbers for your position and education level.

-

2Look into different careers. You can research online to find out how much you would earn doing different kinds of jobs.[5] Look up a particular job or industry that interests you. See what the typical salary is for entry-level jobs in that industry. You can also learn about benefits like healthcare and tuition reimbursement. Also, you can compare what you would earn in different parts of the country.[6] [7]

-

3Figure out how much you're worth. If you have taken the time to research what others are earning doing the same kind of work as you are, compare this to the total annual salary you calculated for yourself. Use this information to negotiate a better salary for yourself. The total amount you can earn depends on many factors, such as your education and years of experience. [8]

- If you are armed with research about how much you could be earning, you might be able to negotiate a better salary. Or, you can ask for a review of your job level or salary based on your qualifications.

References

- ↑ http://www.accountingtools.com/questions-and-answers/what-is-the-difference-between-salary-and-wages.html

- ↑ http://www.hourlysalaries.com/

- ↑ http://www.salary.com/types-of-bonuses/

- ↑ http://www.gcflearnfree.org/careerplanningandsalary/salary-basics/full

- ↑ http://www.salary.com/

- ↑ http://www.myplan.com/index.php

- ↑ http://www.careeronestop.org/JobSearch/Interview/negotiate-your-salary.aspx?&frd=true

- ↑ http://www.gcflearnfree.org/careerplanningandsalary/salary-basics/full

About This Article